Tax Lien vs. Tax Deed: Key Differences Every Investor Must Know

Most people who start researching alternative real estate investing eventually land on two related but fundamentally different strategies: tax lien investing and tax deed investing. Both involve delinquent property taxes. Both are government-backed. And both are regularly misrepresented in the same breath — as if they were the same thing with different names.

They are not. The mechanics are different. The risk profiles are different. The returns come from different places. And the states that allow each strategy are different. Treating them as interchangeable is one of the most common mistakes new investors make, and it leads to real money lost on properties they did not fully understand before bidding.

This guide explains exactly how each strategy works, where the differences matter most, how to identify which states offer which, and — when you have that clarity — how to decide which one fits your investment goals. No fluff. No shortcuts. The full picture.

New to Tax Lien Investing? If you're still building your foundation, start with our free introductory guide before diving into the lien vs. deed comparison. → Read: How to Invest in Tax Liens — The Complete Beginner's Guide |

What Are Tax Liens and Tax Deeds? (A Plain-English Overview)

Before comparing them, both strategies need a clear definition. The confusion between them is not just semantic — it shapes every decision you make at auction, from the state you target to the due diligence you perform.

How Tax Lien Certificates Work

When a property owner fails to pay their property taxes, the local government places a legal claim — a tax lien — against the property. To recover those unpaid taxes without waiting for the owner to pay or foreclosing immediately, most counties in tax lien states sell that lien to private investors at a public tax lien auction.

When you purchase a tax lien certificate, you are not buying the property. You are buying the government's right to collect the debt, plus interest. The property owner then has a legally defined redemption period — typically one to three years, depending on the state — to repay you the face amount of the lien plus statutory interest. If they do not pay, you gain the right to initiate foreclosure and potentially take ownership of the property.

The investment case for tax liens rests on two outcomes: the owner redeems and you earn your interest return, or the owner does not redeem and you acquire a property secured by real estate. The majority of liens — typically 95% or more — are redeemed before foreclosure is necessary.

How Tax Deeds Work

In tax deed states, the county does not sell the lien to investors. Instead, after a delinquency period, the county takes ownership of the property itself through a legal process and then sells that property directly at a tax deed auction. When you buy at a tax deed auction, you are buying the property outright — not a certificate that gives you a claim on it.

The title you receive is called a tax deed or tax collector's deed. In most states, purchasing at a tax deed sale gives you a property free and clear of back taxes owed. However, title issues, surviving encumbrances, and the physical condition of the property are all your responsibility from the moment the auction closes.

Tax deeds are a direct property acquisition play. The return is not a fixed interest rate — it comes from what you do with the property after you buy it: resell it, rent it, rehabilitate it, or in some cases, simply sell it at market value after clearing up the title.

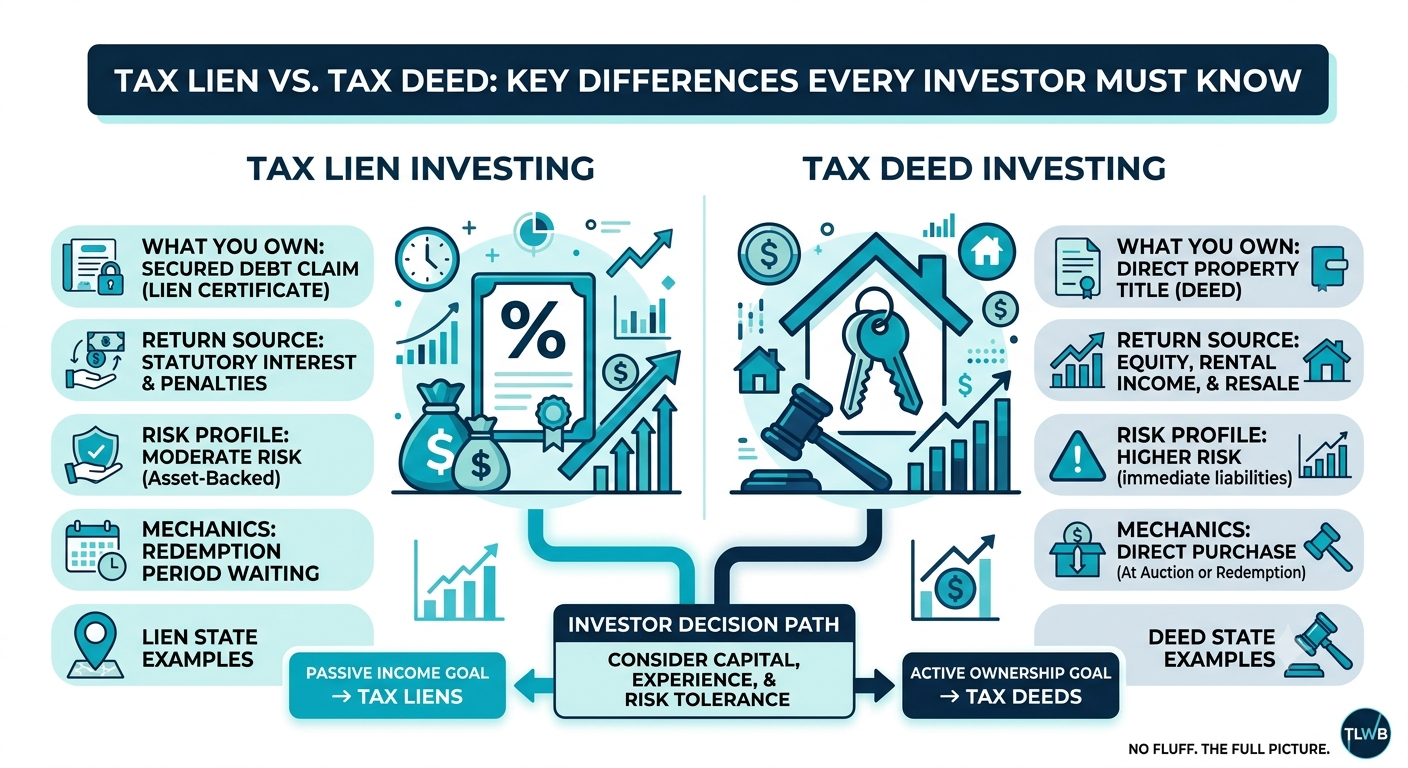

Tax Lien vs. Tax Deed: The Core Differences

The table below summarizes the most important distinctions. Each one is explored in detail in the sections that follow.

Feature | Tax Lien | Tax Deed |

What you buy | A legal claim (certificate) | The property itself |

How you earn | Fixed statutory interest | Resale, rental, rehab profit |

Ownership on purchase | No — lien on the property | Yes — title transfers at auction |

Yes — owner can repay you | Generally no (or very short) | |

Typical hold time | 1–3 years | Immediate (or rehab timeline) |

Capital required | Can be very low (small liens) | Typically higher (full bid) |

Due diligence focus | Property value vs. lien amount | Title, condition, encumbrances |

State availability | ~30 states | ~25 states (some hybrid) |

Worst-case outcome | Foreclosure on bad collateral | Buying unmarketable property |

Competition type | Bid-down interest rate or premium | Bid-up price at auction |

What You Actually Buy

This is the fundamental distinction. In a tax lien state, you purchase a certificate — a document that proves you own the government's claim against the property. You have a senior lien position ahead of nearly all other creditors, including mortgage holders, but you do not own the property. You own the debt.

In a tax deed state, you purchase the property. The auction transfers ownership to the highest bidder. There is no certificate, no interest rate, no redemption period to wait through. The transaction is more like a conventional real estate purchase — compressed into an auction format — than a lending or debt investment.

How You Make Money

Tax lien returns come from statutory interest rates set by each state. These range from 8% in some states to 36% in states like Illinois. The rate is the ceiling — not your guaranteed return. Competition at tax lien auctions drives actual returns down through bid-down interest or premium bidding, depending on the state's auction format. For a detailed breakdown of how those returns are actually calculated, see our guide on how tax lien investing yields high profits.

Tax deed returns are entirely market-dependent. You buy below market value (ideally), then resell at or above market value. The spread between what you paid at auction and what the property is worth — or what you can sell it for after any improvements — is your return. There is no floor. There is no guaranteed interest. Your return is determined entirely by your acquisition price, your due diligence, and your exit strategy.

Risk Profile and Worst-Case Scenarios

Both strategies carry risk. The risks are simply different in character.

For tax lien investors, the primary risk is buying a certificate on a property whose value is less than the amount of the lien plus anticipated foreclosure costs. If the owner never redeems and you initiate foreclosure, you could end up owning a property worth less than you paid. Environmental contamination, structural damage, and competing superior liens are the most serious forms of this risk.

For tax deed investors, the primary risks are title defects, surviving encumbrances (federal tax liens, in particular, can survive a tax deed sale), and condition unknowns. Buying a property at auction that you cannot see inside, and then discovering significant structural problems, is a real outcome for unprepared buyers. This is why thorough due diligence before bidding is not optional in either strategy — but the type of diligence you perform is completely different.

Time Commitment and Redemption Periods

Tax lien investing is a longer-cycle strategy. Redemption periods of one to three years mean that your capital is tied up while you wait for the outcome. You are not actively managing the property during that time, but you are also not liquid.

Tax deed investing is faster in terms of acquisition — you own the property the day the auction closes. But depending on your exit strategy (rehab, resale, rental), your actual time to return can be shorter or longer than a tax lien cycle. If you are targeting quick resales of raw land or simple properties, tax deed investing can move quickly. If you are rehabbing a structure, your timeline extends considerably.

Want to See Both Strategies in Action? Our free live events walk through real tax lien and tax deed examples with experienced instructors. No sales pitch — substantive education. |

Tax Lien States vs. Tax Deed States vs. Hybrid States

The United States does not have a single national tax sale system. Every state sets its own rules. Understanding which category your target state falls into is the starting point for any tax lien or tax deed investment — because the strategy, due diligence, and auction format are all different depending on that classification.

Tax Lien States

In these states, the county sells the right to collect the delinquent taxes as a certificate to private investors. The property owner retains possession during the redemption period and can redeem the lien by paying the face amount plus all accrued interest. If the owner does not redeem, the certificate holder can file for tax lien foreclosure.

Key tax lien states include Florida, Illinois, Arizona, Colorado, Maryland, and New Jersey. Each has a different statutory interest rate, redemption period length, auction format, and foreclosure process. The rules are set at the county level within each state, which adds another layer of variation.

For a state-by-state comparison of rates and rules, see our guide to the best states for tax lien investing.

Tax Deed States

In these states, the county forecloses on the property and takes title before selling it at auction. The buyer at the tax deed sale receives the property — not a lien certificate. There is generally no redemption period after the sale (though the pre-sale notice period exists for the owner).

Key tax deed states include California, Michigan, Texas (which has its own redeemable deed variant), Nevada, Oregon, and Washington. Competition and pricing dynamics differ significantly between states because property markets and starting bid rules vary.

Hybrid (Redeemable Deed) States

Some states use a hybrid system that sits between the two. Redeemable tax deeds are the most common variant: the county sells the deed at auction, transferring the property to the buyer, but the original owner retains the right to redeem within a defined period (often six months to two years). If the owner redeems, you receive the amount you paid plus a statutory penalty.

Texas, Georgia, and Tennessee are the most notable hybrid states. These systems carry characteristics of both strategies — you get the property immediately (deed state characteristic), but you may not be able to do anything with it for months while waiting to see whether the owner redeems (lien state characteristic).

How Returns Are Generated in Each Strategy

Understanding the mechanics of how each strategy produces a return — and under what conditions those returns are reduced or eliminated — is what separates prepared investors from those who learn these lessons the hard way.

Tax Lien Returns: Interest, Penalties, and Redemption

The return on a tax lien certificateA legal document issued by a government authority when a property owner fails to pay property taxes, granting the certificate holder a lien on the property. comes from the interest the owner pays when they redeem. The statutory interest rate is set by state law and applied to the face value of the certificate. In Florida, for example, the rate is capped at 18%, with a minimum 5% guaranteed regardless of how low it was bid at auction. In Illinois, the rate is 36% on the face amount of the penalty.

At most tax lien auctions, investors compete by bidding down the interest rateAn auction format where investors compete by accepting progressively lower interest rates on a tax lien certificate, with the lowest bidder winning. (in states like Florida and Arizona) or by bidding up the premium paid above the lien face value (in states like New Jersey). Either mechanism compresses actual returns below the statutory ceiling. Investors who show up without understanding which auction format the county uses — and where competitive rates typically settle — consistently overbid.

There is also a time dimension: if the lien redeems in month two of a three-year redemption period, you earned two months of interest, not three years. Annualizing your return requires tracking actual hold time, not statutory rate, which is why tax lien portfolio management requires discipline and a system, not just intuition.

Tax Deed Returns: Acquisition, Resale, and Rental

Tax deed returns are the classic real estate investor's calculation: buy below market, generate value, sell or hold above cost. The difference from conventional real estate is the acquisition mechanism — and the risks that mechanism introduces.

The acquisition price advantage comes from the fact that motivated sellers (the county) are not trying to maximize price — they are recovering unpaid taxes. Starting bids are often set at the outstanding tax amount, which can be a fraction of market value. That discount is real. It is also why competition at tax deed auctions in desirable markets is intense, and properties in high-demand areas often sell near or at market value.

For investors using a self-directed IRAAn individual retirement account that allows investment in alternative assets like tax liens and tax deeds for potential tax-advantaged returns. or other tax-advantaged structure to invest in real estate tax strategies, see our post on the function of self-directed IRAs in real estate for a breakdown of how the structure affects both tax liens and tax deeds.

Learn the Numbers Before You Bid Understanding auction formats, return calculations, and due diligence frameworks is what our 3-Day Workshop is built around. See the full curriculum. |

Which Strategy Is Right for You?

This is the question most investors want answered first. It is also the one that requires the most context to answer honestly. The right strategy depends on your capital, your timeline, your risk tolerance, and your bandwidth for active work. Here is the clearest breakdown possible.

Choose Tax Liens If…

Your priority is passive, interest-based income. Tax liens pay a fixed statutory rate. If the owner redeems — which most do — your return is predictable. You are not managing properties, tenants, or contractors.

Your starting capital is limited. You can begin buying tax lien certificates for a few hundred dollars in some counties. The minimum bid is the outstanding tax amount, not the property's value.

You want government-backed security. Your lien holds a senior legal position on the property. The government enforces the rules. No other creditor can pay you out without also paying your interest.

You have patience for a multi-year hold. Redemption periods of one to three years mean your capital is committed. If you need liquidity, this model requires careful planning.

You prefer minimal property management. You do not own the property and are not responsible for it during the redemption period. The owner maintains it (or neglects it — which is a risk to monitor, not a responsibility).

Choose Tax Deeds If…

You want direct property ownership. The auction closes and the property is yours. No waiting for a redemption period to expire before you can act.

You have real estate experience or a strong team. Tax deed investing rewards buyers who understand property valuation, title research, and local real estate markets. It penalizes those who do not.

You are targeting larger capital gains. The spread between a tax deed acquisition price and market value — when your due diligence is solid — can be substantial. Interest rates cannot compete with a well-researched tax deed in an appreciating market.

You can deploy capital quickly. Tax deed auctions require payment immediately or within a short window. You need liquid capital ready before you bid.

You understand title risk. Tax deed title can carry surviving encumbrances. Federal tax liens, in particular, do not always get extinguished by a tax deed sale. A title search and potentially title insurance are not optional steps for serious tax deed investors.

A Note on Hybrid States

If you are investing in a redeemable tax deed state, your decision framework shifts. You have immediate possession in the sense that the deed transfers at auction, but the former owner's right of redemptionThe legal right of a property owner to reclaim their property after a tax sale by paying the full amount of delinquent taxes, interest, and penalties. limits what you can do with the property during that window. For investors who want to start work on a property immediately, redeemable deed states require special planning.

United Tax Liens offers a complementary online training program that covers both lien and deed strategies across multiple states — worth reviewing if you are exploring markets outside your current geography. See unitedtaxliens.com for their current course offerings.

Common Mistakes Investors Make When Choosing Between the Two

These are not theoretical errors. They are patterns observed across thousands of first-time and intermediate investors who approached one strategy while mentally operating in the framework of the other.

Confusing the State Type

Showing up at a county sale expecting to bid on lien certificates — because you did your research on Florida — and discovering that the county is selling properties outright is a real scenario. State classification is the first thing to verify before any research, not an afterthought.

Use our state-by-state resources to confirm whether your target state is a lien state, deed state, or hybrid before proceeding with any county-level research.

Ignoring Due Diligence Requirements

Due diligence in tax lien investing focuses on the property's value relative to the lien amount and the presence of environmental issues or superior encumbrances. Due diligence in tax deed investing adds title research, structural condition assessment, and often a comparison of the auction price against detailed comparable sales data. These are different processes. Applying lien-level diligence to a deed purchase — or skipping it entirely — is where serious financial damage happens.

Underestimating Foreclosure Timelines

Investors who buy tax liens expecting to acquire properties through tax lien foreclosure frequently underestimate how long and how costly that process is. Foreclosure timelines vary by state from as little as several months to over two years. Legal fees, filing costs, and carrying costs during that period reduce the return substantially. The math only works if the property's value justifies it — which is why the initial due diligence on the collateral matters so much more than most first-time buyers expect.

How to Research Tax Lien and Tax Deed Opportunities

Research is the job. The auction is just the result of research done well or poorly. Here is what that research actually looks like in practice.

Researching County-Level Rules

Start with the state classification, then move to the county. Within a given lien or deed state, individual counties set their own auction dates, registration requirements, payment timelines, and in some cases their own interest rate structures within the statutory range. The county treasurer's or tax collector's website is the primary source — not third-party aggregators, which are frequently outdated.

The questions to answer before any county auction: What is the auction format (bid-down rate, bid-up premium, bid-up price)? When do auctions run? What is the registration process and deposit requirement? What is the redemption period length? Are online auctions available, or is the sale in-person only?

Evaluating the Underlying Property

For tax lien certificates, the core question is: if this owner does not redeem and I have to foreclose, is the property worth more than my total costs — certificate purchase price, interest carrying costs, foreclosure legal fees, and any outstanding superior liens? If the answer is yes, the lien has real collateral backing and is worth pursuing. If the answer is no or uncertain, pass.

For tax deeds, the question is: what can I realistically sell or rent this property for, and what does it take to get there? Use comparable sales data from the county assessor's records, cross-reference with public listing data, and verify the physical condition as best you can before bidding. For a primer on evaluating real estate investment fundamentals, see our How It Works overview.

Online Auctions vs. In-Person Auctions

An increasing number of counties have moved to online platforms — RealAuction, Bid4Assets, and county-specific portals are the most common. Online auctions increase tax lien auction competition because geographic barriers disappear. The upside is that you can participate in multiple states without traveling. The downside is that the same accessibility applies to every other investor, which typically compresses available returns in high-demand counties.

In-person auctions in smaller counties — particularly in rural areas — remain less competitive. Investors willing to put in the logistical effort of attending in-person sales sometimes find better returns than comparable online markets, though the properties themselves may also carry more uncertainty.

Want Expert Guidance on Research and Due Diligence? Our Mastery Program covers county-level research systems, due diligence frameworks, and live auction practice. See what's included. |

Building a Portfolio With Both Strategies

Experienced investors frequently use both tax liens and tax deeds as part of a broader investment portfolio — not because variety is inherently good, but because each strategy's risk and return profile serves different portfolio goals at different stages.

Diversifying Across States and Strategy Types

Holding tax lien certificates in Florida and Arizona while pursuing tax deed acquisitions in Michigan, for example, combines a passive interest income stream from the liens with active equity-building through the deeds. The lien portfolio provides predictable quarterly or annual returns; the deed acquisitions provide irregular but potentially higher capital gains.

This kind of cross-state, cross-strategy approach requires a tracking system and a clear understanding of the rules in each jurisdiction. It is not a beginner's starting point. If you are new, the consistent advice from experienced investors is: master one state and one strategy type before adding complexity. See our success stories to see how investors at different experience levels have built their portfolios.

Tracking Redemption Periods and Deadlines

The mechanics of a tax lien portfolio — monitoring redemption deadlines, calculating when foreclosure rights become available, tracking which liens have been paid off — require systematic record-keeping. Missing a foreclosure filing deadline means losing your right to foreclose and potentially losing the certificate's value.

This is one of the operational realities of tax lien investing that is frequently omitted from introductory materials. The strategy is passive in the sense that you do not manage a property, but it is not passive in the sense that you can ignore it. Active monitoring of your certificate portfolio is part of the job. Our free introductory event covers portfolio management basics as part of the standard curriculum.

Frequently Asked Questions

Is tax lien investing safer than tax deed investing?

Neither strategy is categorically safer. Tax liens offer government-backed security on the certificate and a senior lien position, but they carry foreclosure risk if the collateral is inadequate. Tax deeds give you immediate property ownership, which is a more tangible asset, but they expose you to title issues, condition unknowns, and market risk. The safety of either strategy comes from the quality of your due diligence, not the label.

Can you invest in both tax liens and tax deeds at the same time?

Yes, and experienced investors often do. The strategies are complementary when managed properly. That said, both require distinct skills, research processes, and auction preparation. Building competence in one before adding the other is the more reliable path to sustainable returns.

What happens if the property owner declares bankruptcy?

Bankruptcy introduces complexity for both strategies. For tax lien investors, a bankruptcy filing triggers an automatic stay that halts foreclosure proceedings. The lien itself is not eliminated — federal law generally protects property tax liens in bankruptcy — but the timeline for resolution extends significantly. For tax deed purchasers, a bankruptcy filed before the deed sale can stop the sale entirely. County attorneys and experienced investors treat active bankruptcies as a separate research category in their due diligence process.

How much money do you need to start?

Tax lien investing has the lower entry point. Small certificates in rural counties can be purchased for under $1,000 — sometimes under $500. That said, a concentrated portfolio of very small liens requires significant monitoring effort for modest returns. Most experienced investors recommend starting with a realistic capital plan that accounts for multiple certificates, carrying costs, and a reserve for potential foreclosure expenses.

Tax deed investing typically requires more capital because you are buying a full property, not a certificate. Starting bids at tax deed auctions in some markets can be below $5,000 for vacant land, but residential properties in competitive markets bid much higher.

Are tax deed titles clean?

Not always. Tax deed titles extinguish most junior liens and claims, but federal tax liens can survive a tax deed sale under certain conditions. Title insurance is often difficult or impossible to obtain immediately after a tax deed purchase, which affects your ability to finance or resell the property quickly. Conducting a thorough title search before bidding — not after — is the professional standard.

Do tax deed auctions require you to pay the full amount immediately?

Rules vary by county and state. Some require full payment the day of the auction; others allow 24–72 hours; some require a deposit at the sale with balance due within 30 days. Verify payment terms for every county you plan to bid in before registering — showing up without knowing the payment requirement is a disqualifying oversight in competitive auctions.

What is a redeemable tax deed and how does it differ?

A redeemable tax deed transfers the property to the buyer at auction, but the original owner retains the right to reclaim it by paying a penalty during a defined redemption period. It combines elements of both strategies: you have a deed (deed state characteristic), but you face a potential redemption and cannot develop or sell the property freely until that window closes (lien state characteristic).

Which strategy generates higher returns?

Neither is universally higher. Tax deeds have the potential for much larger absolute returns on individual properties — a $10,000 acquisition later sold for $60,000 is not uncommon in the right market. Tax liens offer more predictable percentage returns, often 8–18% annualized in competitive markets, without the property management exposure. Comparing them on returns alone misses the more important question: which one fits your skills, capital, and time commitment?

Can I invest in tax liens or tax deeds using an IRA?

Yes, through a self-directed IRA (SDIRA). Both strategies are permissible investments within an SDIRA, provided you follow the rules around prohibited transactions and maintain proper separation between your IRA funds and personal funds. The mechanics of using an SDIRA for either strategy are covered in detail in our post on the function of self-directed IRAs in real estate investing.

How do I find tax lien and tax deed auctions near me?

Start with the county treasurer's or tax collector's website for your target jurisdiction. Most counties publish their upcoming auction schedules, registration requirements, and available properties online. For a structured introduction to the research process, our free live events walk through auction identification and preparation with experienced instructors in a classroom setting.

Conclusion

Tax liens and tax deeds are not the same strategy with different names. They are different instruments, with different mechanics, different risk profiles, and different research requirements. The county that sells lien certificates in one state may sell properties outright in the next. The due diligence that protects you in a deed auction is not the same as the due diligence that protects you when buying a tax lien certificate.

What the two strategies share is that they both reward preparation. The investors who consistently generate strong returns in either category are the ones who did the research before bidding — on the state rules, on the county format, on the specific property, and on the numbers that make an individual investment worth pursuing. Preparation is not a differentiating factor. It is the baseline.

If you are deciding where to start, the clearest path is: pick one state, master its rules, and build from there. Our beginner's guide to tax lien investing is the right starting point if you are new to the space. If you are ready for structured instruction and real-world auction practice, our free live events and 3-Day Workshop are built for exactly that.

The strategy is real. The discipline it requires is also real. Both are manageable for investors who approach this with the right preparation.

Ready to Start? Attend a Free Live Event Tax Lien Wealth Builders hosts free introductory events across the US. No obligation, no sales pressure — expert education on both tax lien and tax deed investing in a classroom format. |

Earnings Disclaimer Results vary. Tax lien and tax deed investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. Nothing in this article constitutes financial, legal, or investment advice. See our full earnings disclaimer before making any investment decisions. |

Related reading: How to Invest in Tax Liens · What Is a Tax Lien · Best States for Tax Lien Investing · How Tax Lien Investing Yields High Profits · Explore Our Blog