Tax Lien Investing: How to Buy Tax Lien Certificates, Properties, and Generate Returns

Tax lien investing has become one of the most discussed alternative real estate strategies for investors looking to generate returns without directly owning property. Unlike traditional real estate investing, where you purchase and manage physical assets, tax lien investing allows you to invest in delinquent property taxes and potentially earn interest or acquire property at a fraction of its value.

If you're exploring purchasing a tax lien certificate this guide will walk you through everything: from fundamentals to advanced strategies. Whether you're asking “how does tax lien investing work” or “is tax lien investing a good idea”, this guide is designed to answer every major question.

What Are Tax Liens and How Do Tax Liens Work?

What is a Tax Lien?

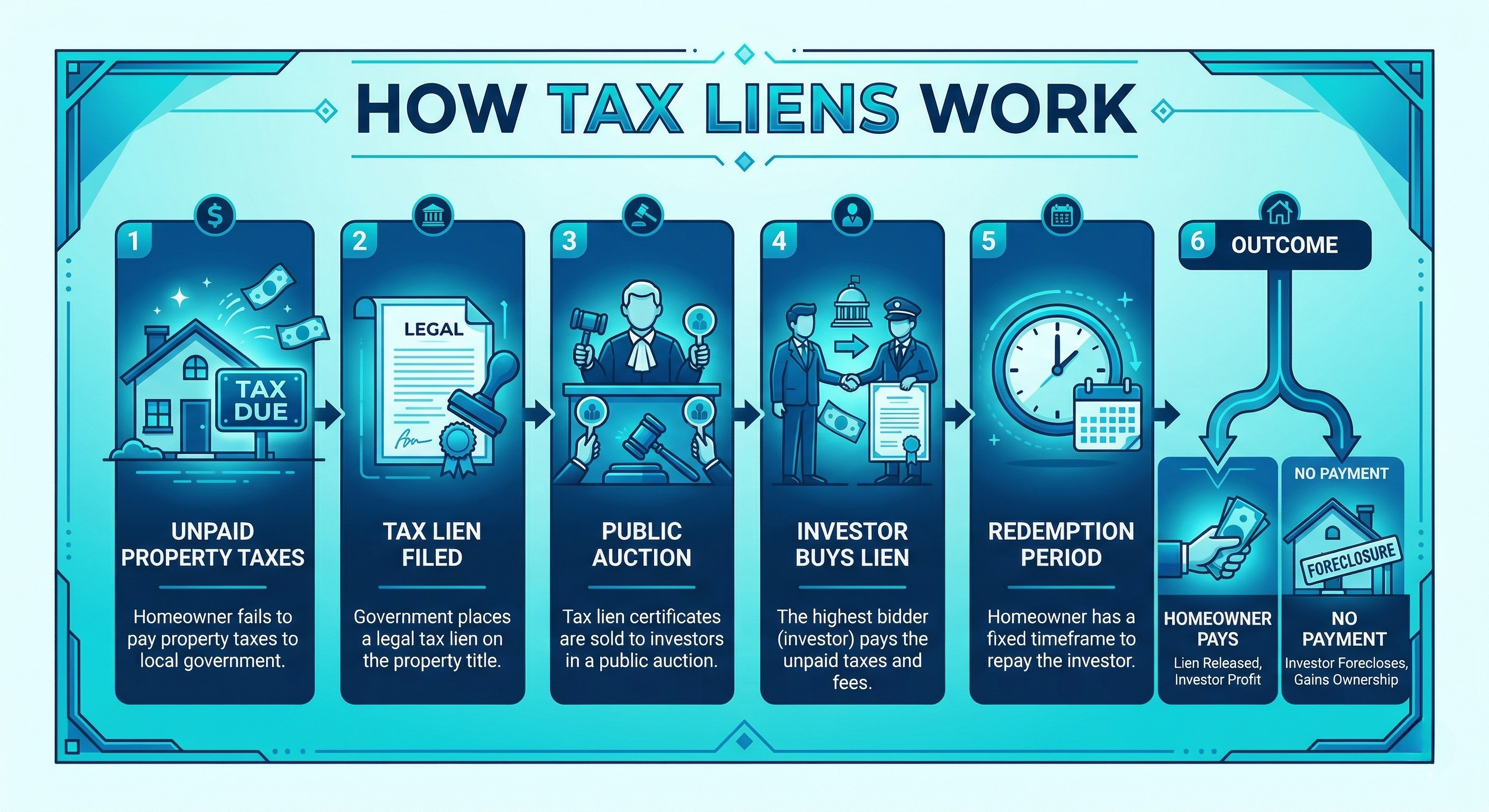

A tax lien is a legal claim the government places on a property when the owner fails to pay their property taxes. It gives the government first priority on that property, ahead of mortgage lenders, other creditors, and anyone else with a financial interest, until the debt is fully resolved.

Here's how it works in practice: when a property owner falls behind on taxes, the local county or municipality doesn't immediately seize the property. Instead, it records a lien against it. That lien does two things. First, it formally documents the debt, including the unpaid taxes, penalties, and accruing interest. Second, it clouds the property's title, meaning the owner cannot sell the property or refinance their mortgage until the lien is paid off. The owner is essentially stuck until the debt is cleared.

This is not a rare situation. Counties across the United States issue hundreds of thousands of tax lien certificates every year, representing billions of dollars in delinquent property taxes. Every state has some version of this process, though the rules, interest rates, and timelines vary.

To recoup the unpaid taxes without going through a lengthy foreclosure process, many counties sell these liens to outside investors. When you purchase a tax lien certificate, you pay the delinquent balance on behalf of the property owner. The county gets its money immediately. The owner now owes that debt to you instead of the government, and they must repay you, with interest, to clear the lien and regain clean title to their property.

That interest rate is set by state law and is often higher than more traditional investments, anywhere from 8% to 36% annually depending on the state. And because the lien is secured by real property, it carries a level of collateral backing that most fixed-income investments cannot offer.

How Are Tax Liens Created

Tax liens don't appear out of nowhere. They follow a defined legal process that counties across the country use to recover unpaid property taxes without resorting to immediate foreclosure. While the specifics vary by state, the general sequence looks like this:

Step 1: Taxes Become Delinquent

Property taxes are typically due once or twice a year. When an owner misses the deadline, the county doesn't act immediately. Most jurisdictions build in a grace period and send notices giving the owner a chance to pay. If the taxes remain unpaid past a certain cutoff, usually several months to over a year depending on the state, the account is officially declared delinquent and the clock starts running.

Step 2: The Government Records a Lien

Once delinquency is confirmed, the county records a formal lien against the property. This becomes part of the public record, visible to anyone who searches the property's title. From this point forward, the owner cannot sell or refinance the property with clean title until the debt is resolved.

Step 3: The Lien Is Packaged Into a Certificate

The recorded lien is converted into a tax lien certificateA legal document issued by a government authority when a property owner fails to pay property taxes, granting the certificate holder a lien on the property., which documents the property address, the amount owed, the penalty rate, and the applicable interest rate set by state law. This certificate is the actual investment instrument that changes hands.

Step 4: The Certificate Is Auctioned to Investors

Counties then offer these certificates for sale, typically through public auctions held online or in person. Depending on the state, investors may bid on the interest rate they are willing to accept or compete to pay a premium above the lien amount. The winning investor pays the delinquent balance in full, the county collects its money, and the investor steps into the government's position as the lien holder.

The system works because both sides get something they need. The county recovers tax revenue immediately without a costly legal battle. The investor acquires a secured, interest-bearing claim backed by real property. The property owner gets time to pay, though the clock is now running against them.

How Do Tax Liens Work in Real Estate

When most people think about real estate investing, they think about buying property. Tax lien investing works differently. You are not purchasing the property itself. You are purchasing the debt secured by that property, and that distinction matters enormously.

The Priority Position

Tax liens carry what is called senior lien status. This means the tax lien sits at the front of the line ahead of nearly every other claim on the property, including the mortgage. If a property has a $200,000 mortgage and a $4,000 tax lien, the tax lien gets resolved first. The bank, despite holding a much larger claim, cannot foreclose or take action until the tax obligation is satisfied. This priority position is established by law, not negotiation, and it is one of the primary reasons tax liens are considered a relatively secured form of investment.

Scenario One: The Owner Pays

This is the most common outcome. The property owner, motivated to clear the lien and regain clean title, pays the redemption amount during the state-mandated redemption period. That amount includes your original investment plus the statutory interest rate, which varies by state but typically ranges from 8% to 36% annually.

To put numbers to it: you purchase a $5,000 tax lien certificate in a state with a 24% annual interest rate. The owner redeems the lien eight months later. You collect your $5,000 back plus roughly $1,600 in interest. You never touched the property. You never dealt with tenants or repairs. You simply waited.

Scenario Two: The Owner Does Not Pay

If the owner fails to pay within the redemption periodThe legally defined timeframe during which a property owner can reclaim their property by paying the delinquent taxes plus interest and penalties., you gain the right to initiate foreclosure proceedings on the property. This is where the conversation around tax liens gets more complicated, and more interesting.

Foreclosure through a tax lien is a legal process that takes time and involves filing costs and court procedures. It is not instant, and it is not guaranteed to be simple. However, if the process completes and no one steps in to redeem the lien, you can potentially acquire the property for the amount you paid at auction, which is often a fraction of its market value.

This outcome is less common than redemption, but it does happen, and it is the scenario that draws many investors to this asset class in the first place.

Not All Tax Liens Are Equal

Before purchasing any certificate, the underlying property matters. A lien on a well-maintained home in a stable neighborhood carries very different risk than a lien on a vacant lot or a structurally compromised building. If you foreclose and the property has little value, the math does not work in your favor. Serious investors research the property before bidding, not after.

Understanding both sides of that equation, the upside of secured interest income and the downside of a property not worth pursuing, is what separates informed tax lien investors from people who learned the strategy from a late-night infomercial.

Tax Lien Investing Explained (Beginner to Advanced)

Tax Lien Investing: What You Actually Need to Know

Tax lien investing is frequently marketed as a form of passive income, and that framing is not entirely wrong. You are not buying physical property, managing tenants, handling repairs, or dealing with the operational headaches that come with traditional real estate. On the surface, the model is simple: purchase a certificate, wait for repayment, collect interest.

But "passive" can be a misleading word if it implies that success requires no real work. It does.

At its core, tax lien investing means purchasing the government's legal claim on a property and stepping into its position as the lien holder. When the property owner repays the debt, you collect your principal plus interest at the rate set by state law. When they do not repay, you gain the right to pursue foreclosure. The financial upside on paper is straightforward. The execution is where investors are separated into two camps: those who treat it as a discipline and those who treat it as a shortcut.

Successful tax lien investing requires you to research the underlying property before you bid, not after. It requires you to understand how auctions work in the specific county you are targeting, because the rules, bidding formats, and interest structures vary significantly from state to state and sometimes county to county. It requires you to understand redemption periods, what triggers them, how long they last, and what your legal obligations and options are during that window. And it requires ongoing monitoring of your certificates, because a lien sitting unresolved is not a set-it-and-forget-it situation.

None of this makes tax lien investing inaccessible. Thousands of investors participate in this market successfully every year. But walking in without that foundation is how people end up holding a certificate on a property that is not worth the paper the lien is printed on.

The investors who do well here treat it as a skill, not a secret.

To that end we offer FREE, In-Person Workshops that will walk you through the entire process, step-by-step. You can click here to see if we are currently in your area right now!

Is Tax Lien Investing Legit?

Yes. Tax lien investing is a legitimate, government-created, and government-administered process that has existed in the United States for well over a century. It is not a loophole, a workaround, or a gray-area strategy. Counties and municipalities across the country depend on this system to recover unpaid property tax revenue without tying up public resources in lengthy foreclosure proceedings. When you purchase a tax lien certificate, you are participating in an officially sanctioned public auction process governed by state law. The transaction is recorded, regulated, and enforceable in court.

So Why Do People Question It?

The skepticism is understandable, and it comes from a specific place: the way tax lien investing has been marketed over the years. For decades it has been a staple of late-night infomercials, weekend seminar circuits, and online guru courses promising properties for pennies on the dollar with almost no risk. That promotional culture has done real damage to the credibility of an otherwise sound investment vehicle. When something sounds too good to be true and is being sold by someone in a rented ballroom, people reasonably question whether the underlying opportunity is real.

The opportunity is real. The exaggerated promises around it often are not.

The Vehicle Is Legitimate. The Execution Is Where It Gets Complicated.

Buying a tax lien certificate is a legal transaction backed by government authority. What is not guaranteed is the outcome. The legitimacy of the process does not protect you from buying a lien on a property with serious title issues, environmental contamination, structural problems, or no realistic resale value. It does not protect you from misunderstanding the redemption rules in a state you have not researched properly. It does not protect you from overpaying at auction in a competitive market where your margin disappears before you ever collect a dollar.

These are not reasons to avoid tax lien investing. They are reasons to approach it the same way you would any serious investment: with due diligence, realistic expectations, and a clear understanding of the rules in the specific jurisdiction where you are operating.

A Note on Regulation and Oversight

Tax lien auctions are subject to state statutes that govern everything from how auctions are conducted to what interest rates are allowed to how long property owners have to redeem their debt. These are not informal arrangements. They are codified processes with legal consequences for both investors and property owners. That regulatory framework is part of what makes this asset class credible and why institutional investors, including hedge funds and large investment firms, have entered the space in significant volume over the past two decades.

The presence of institutional capital in tax lien markets is itself a form of validation. These are not organizations that participate in illegitimate schemes.

The Bottom Line

Tax lien investing is legitimate. It is also not for people looking for a passive shortcut or a guaranteed return. Approached with the right preparation, it can be a disciplined, interest-generating strategy with real collateral backing it. Approached carelessly, it can leave you holding a certificate on a property worth less than what you paid for the lien. The process is sound. The results depend entirely on the investor.

How to Buy Tax Lien Certificates (Step-by-Step)

Buying a tax lien certificate is not complicated once you understand the process. But "not complicated" does not mean "no preparation required." The investors who struggle are almost always the ones who showed up to an auction before they understood what they were bidding on, how the auction worked, or what they would do if the property owner never paid. This section walks through the full process so you enter the market with a clear picture of what you are actually doing.

Step 1: Choose Your Target State and County

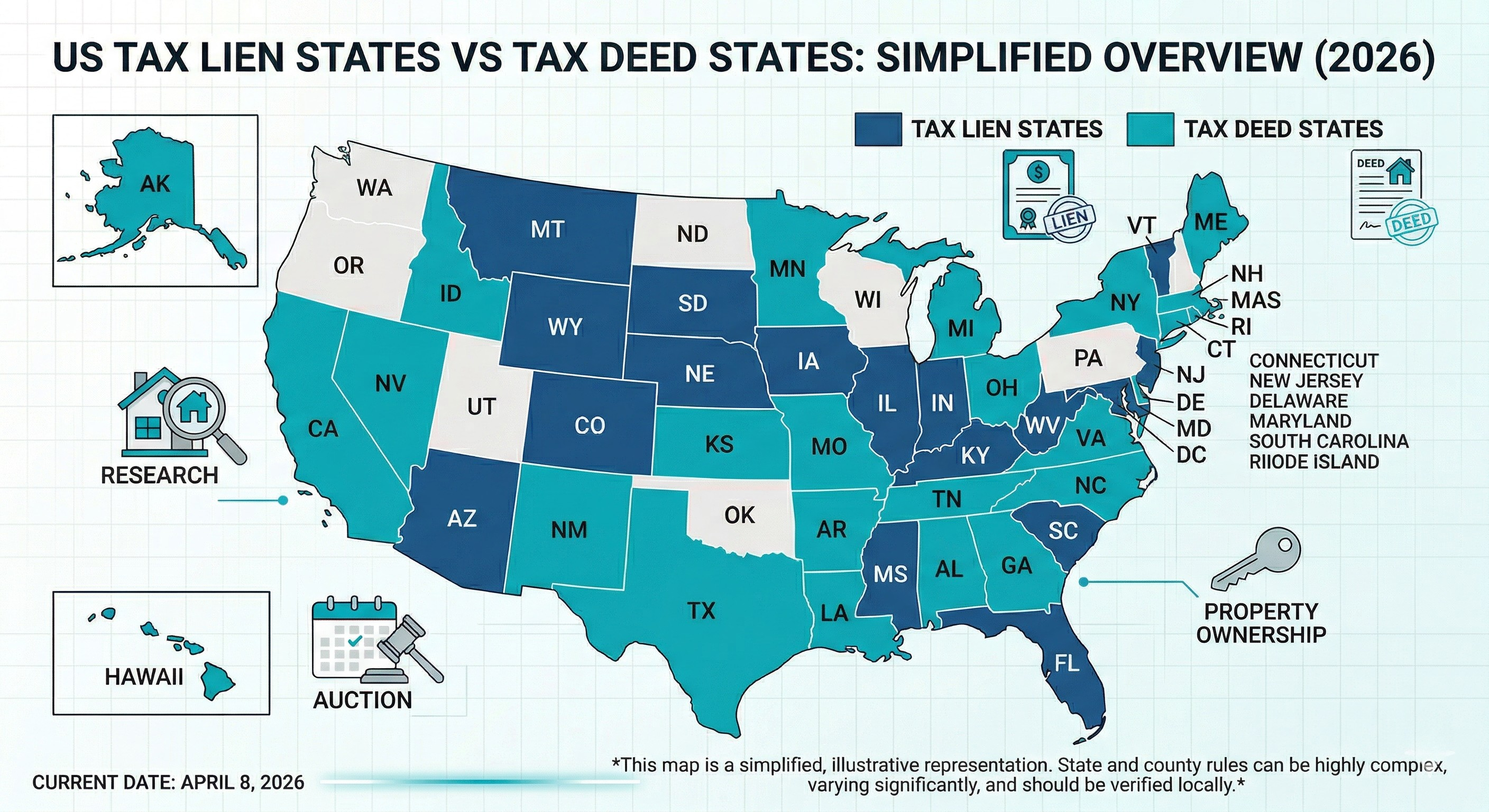

Not all tax lien states are created equal. Twenty-one states plus Washington D.C. are considered tax lien states, meaning they sell lien certificates to investors. The remaining states use a tax deed system, which works differently. Before anything else, you need to confirm that the state you are targeting operates a lien system, not a deed system.

From there, the differences between states become significant. Interest rates vary from as low as 8% annually in some states to as high as 36% in others. Redemption periods, which determine how long a property owner has to repay before you can initiate foreclosure, range from a few months to several years. Some states are investor-friendly with well-organized auction systems and clear statutes. Others have processes that are harder to navigate, especially for newcomers.

Picking the right state to start in is a strategic decision, not an afterthought. Study the interest rate structure, redemption timeline, foreclosure process, and how competitive the auction environment tends to be before you commit to a market.

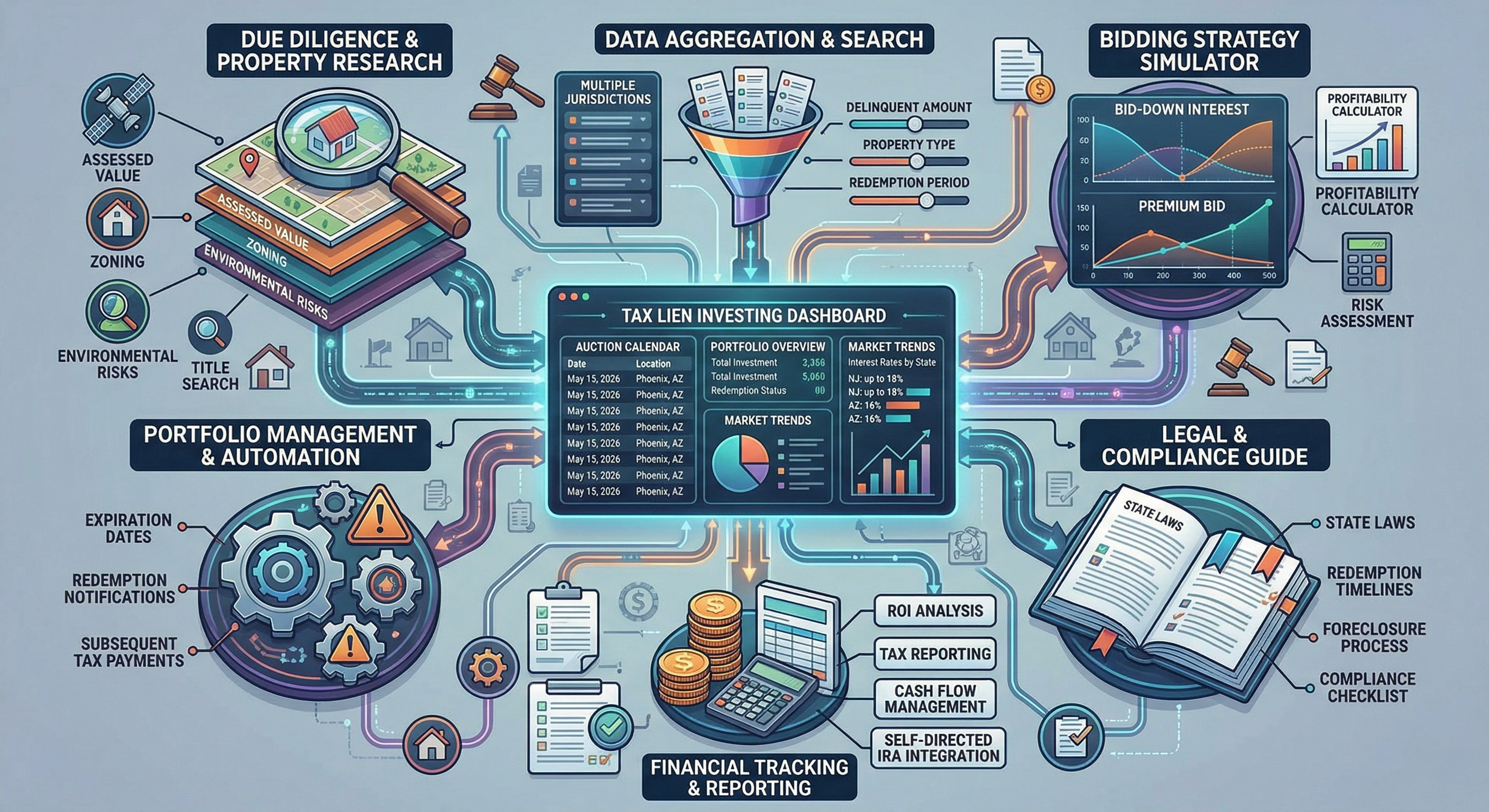

Step 2: Research Available Liens Before the Auction

Most counties publish a list of available tax lien certificates in advance of the auction, either in a local newspaper, on the county website, or through the county treasurer or tax collector's office. This list is your starting point.

Or if you are part of the Tax Lien Wealth Builders community you will have access to our proprietary Tax Lien Software, MarketPlacePro.

For every certificate you are considering, you need to research the underlying property before you bid. This is not optional. The lien is only as good as the asset behind it, and a lien on a property with no value is a problem regardless of the interest rate attached to it.

Your pre-auction research should include:

Assessed value relative to the lien amount. If a property is assessed at $150,000 and the lien is $3,500, that is a very different risk profile than a lien of $3,500 on a property assessed at $8,000. You want a meaningful cushion between what you are paying and what the property is worth.

Title search. Look for other liens or encumbrances on the property. A federal tax lien, for example, may survive your purchase depending on the state, which can complicate your position significantly. Junior liens typically get wiped out in a tax lien foreclosure, but senior liens do not, and federal liens sit in a special category. Know what else is attached to a property before you buy.

Physical condition and location. Drive by the property if it is local, or use satellite imagery and street-level tools if it is not. A vacant lot, a condemned structure, or a property in a severely depressed area carries real risk. If you end up needing to foreclose, you want to own something worth owning.

Ownership history and delinquency pattern. A property that has been delinquent multiple times may signal a pattern. It may also mean other investors have already looked at it and passed.

Step 3: Register for the Auction

Whether the auction is in person or online, counties require investors to register in advance. Registration requirements vary but typically include submitting identifying information, completing any required forms, and in many cases depositing funds or providing proof of funding capacity before you are permitted to bid.

Do not underestimate the administrative side of this. Deadlines for registration and deposit submission are firm. Missing them means missing the auction entirely. Contact the county treasurer or tax collector's office early to confirm requirements, and read the auction rules carefully because counties do not make exceptions for people who did not read the instructions.

Step 4: Understand the Bidding Format Before You Bid

This is where many new investors make expensive mistakes. Auction formats differ significantly by state, and bidding the wrong way in the wrong format can result in overpaying or walking away with a lien that earns you almost nothing.

The three most common bidding formats are:

Bid down the interest rate. In states like Florida and Arizona, investors compete by bidding down the interest rate they are willing to accept. The lien starts at the maximum statutory rate and investors bid lower until no one will go lower. The investor willing to accept the lowest rate wins the certificate. In highly competitive markets, rates can be bid down dramatically, sometimes to near zero, which significantly reduces your return.

Premium bidding. In some states, the interest rate is fixed and investors compete by paying a premium above the lien amount. The highest premium wins. The problem with premium bidding is that you pay more than the lien amount, but if the property owner redeems, they only pay the base lien plus interest, not your premium. You absorb that difference. Calculating whether a premium bid still makes financial sense requires careful math before you bid.

Rotational or random assignment. Some counties use lottery or rotational systems where qualified investors are assigned liens rather than competing in open bidding. These systems can be favorable for newer investors because they reduce the impact of competitive pressure.

Know which system you are entering before auction day. The strategy you use in a bid-down state is completely different from the one you use in a premium-bid state.

Step 5: Bid With Discipline, Not Emotion

Auctions create pressure. Whether you are sitting in a county courthouse or watching numbers move on a screen, it is easy to get caught up in the momentum and overbid. Set your maximum acceptable return before the auction starts and do not deviate from it.

If you are in a bid-down state, know the minimum interest rate you are willing to accept before you enter the room. If you are in a premium-bid state, calculate the maximum premium you can pay and still earn a return that justifies the investment. Walk away from any certificate where the math stops working, regardless of how much time you spent researching it.

The discipline to pass on a bad deal is just as important as the skill to identify a good one.

Step 6: Complete the Purchase and Secure Your Certificate

Once you win a certificate, you are typically required to pay in full quickly, sometimes the same day, sometimes within 24 to 72 hours depending on the county. Failure to pay forfeits your winning bid and may result in penalties or disqualification from future auctions in that jurisdiction.

Payment methods vary by county. Some accept checks, some require wire transfers, and online platforms typically process payment through their own systems. Confirm accepted payment methods before auction day.

After payment, the county issues your tax lien certificate, which documents the property address, lien amount, interest rate, and relevant dates. Keep this document secure. It is the legal instrument that represents your investment.

Step 7: Monitor Your Certificates Through the Redemption Period

Buying the certificate is not the end of your work. During the redemption period, you need to track your liens and understand what is happening with each property. Most counties will notify you if a lien is redeemed, but not all do so reliably. Build a simple tracking system that documents each certificate, the redemption deadline, any required actions on your part, and the status of payment.

In some states, you are required to send notice to the property owner at certain points during the redemption period or before initiating foreclosure. Missing these notice requirements can invalidate your ability to foreclose, so understand your obligations and calendar them in advance.

Step 8: Collect Your Return or Pursue Foreclosure

When the owner redeems the lien, the county processes the repayment and you receive your principal plus interest. In most cases this happens without any direct interaction between you and the property owner.

If the redemption period expires without payment, you have the right to initiate foreclosure proceedings. This involves filing with the appropriate court, serving required notices, and moving through a legal process that varies in length and complexity by state. You will likely incur legal fees during this process. Factor those into your overall return calculation.

If foreclosure completes successfully and no one redeems the property, you may acquire the title at a cost that reflects only what you paid for the lien plus your foreclosure expenses. Whether that outcome is favorable depends entirely on the value of the property and what you plan to do with it.

Due Diligence: The Step That Cannot Be Skipped

Every step above depends on the quality of your research before you bid. Due diligence in tax lien investing is not a checklist you complete to feel responsible. It is the actual work that determines whether your investment performs or becomes a problem.

A thorough due diligence process covers:

Property valuation. Use county assessment records, comparable sales data, and where possible, a physical review of the property. The assessed value is a starting point, not a final answer. Assessed values can lag market conditions significantly.

Title review. Pull the full title history and look for anything that could survive your lien or complicate a future foreclosure. Federal tax liens, IRS liens, and certain environmental claims require extra scrutiny.

Property condition. Beyond the value question, you need to understand what you would be acquiring if you had to foreclose. A property with foundation issues, fire damage, or code violations is a liability, not an asset.

Market context. A property is worth what someone will pay for it in the current market. Research the neighborhood, recent sales activity, and demand before assuming a high assessment means a strong asset.

Redemption likelihood. This is harder to quantify, but experience helps. Owner-occupied properties with mortgages tend to redeem at higher rates because the owner has something to lose. Vacant lots and investment properties with absentee owners carry higher foreclosure risk, which may be an opportunity or a complication depending on what the property is worth.

The investors who build consistent returns in this asset class are not the ones who found some secret strategy. They are the ones who do the research every time, on every certificate, without exception.

How to Buy Property with Delinquent Taxes

Let's address the most common misconception up front: paying someone's back taxes does not hand you the keys to their house. The process is more structured than that, more patient than that, and in most cases, it does not end in property ownership at all. Understanding this from the start will save you from the frustration that comes with misaligned expectations.

When you purchase a tax lien certificate, you are buying a secured legal claim against a property, not the property itself. The path from that certificate to actual ownership is real, but it runs through a specific legal process that takes time, requires compliance with state statutes, and is never guaranteed to produce a deed in your name.

What "Delinquent Taxes" Actually Means for the Property

When a property owner stops paying taxes, the county does not immediately move to take the property. The government's first priority is recovering the revenue, not acquiring real estate. That is why the tax lien system exists. By selling the lien to an investor, the county gets its money now and transfers the collection risk to you.

The delinquency itself has real consequences for the owner. The lien clouds the title, freezing their ability to sell or refinance. Interest and penalties accumulate on the unpaid balance. And the clock on the redemption period begins running, counting down toward the point where the investor gains the legal right to pursue foreclosure.

For the owner, this creates powerful motivation to pay. For you as the investor, it means that most of the time, you will collect interest rather than a deed. Nationwide, redemption rates on tax lien certificates are high, often cited in the range of 95% or better depending on the state and property type. The foreclosure outcome, while possible and sometimes lucrative, is the exception rather than the rule.

The Redemption Period: What It Is and Why It Matters

Every state that operates a tax lien system grants the property owner a legally defined window of time to repay the debt before the investor can move toward foreclosure. This is called the redemption period, and it varies significantly by state.

Some states set redemption periods as short as six months. Others extend them to two or even three years. During this window, the owner can pay the outstanding lien amount plus the accrued interest and any applicable penalties, and the lien is extinguished. You receive your principal and interest, and the transaction is complete.

The length of the redemption period matters for your investment timeline and your capital planning. A two-year redemption period in one state means your capital is tied up for potentially two years before you know whether you are collecting interest or pursuing foreclosure. A six-month period in another state moves much faster. When choosing your target market, the redemption timeline should be part of your evaluation alongside the interest rate and auction format.

During the redemption period, you are not passive in all states. Some jurisdictions require you to send formal notice to the property owner at specific intervals, informing them of the outstanding lien and the approaching deadline. Failing to send required notices at the right time and in the right format can legally invalidate your ability to foreclose, even if the owner never paid a cent. Know your obligations, calendar every deadline, and treat compliance as non-negotiable.

What Happens When the Owner Does Not Pay

If the redemption period expires without payment, you gain the legal right to initiate foreclosure proceedings. This is the moment many investors have been waiting for, but it is important to understand what you are entering before you file.

Tax lien foreclosure is a court-supervised legal process. It is not a simple administrative step. The general sequence looks like this:

You file a foreclosure action with the appropriate court in the county where the property is located. The filing initiates the formal legal process and establishes your claim on the record.

The property owner and any other parties with a legal interest in the property, including mortgage holders, junior lienholders, and sometimes tenants, must be formally notified. This service of process requirement exists to give all interested parties a chance to respond, redeem the lien, or contest the action.

A waiting period follows during which those parties can respond. In many states, the owner retains the right to redeem the lien even after foreclosure is filed, up until a certain point in the proceeding. Do not assume that filing ends the possibility of redemption.

If no one redeems and the court finds in your favor, a judgment is entered and the property moves toward a tax deed or sheriff's sale depending on the state's process. At that point, you may acquire title directly or through a subsequent auction.

The entire foreclosure process can take anywhere from a few months to well over a year depending on the state, the court's caseload, and whether the action is contested. You will also incur legal fees, court costs, and potentially title search and service of process expenses. Build those costs into your numbers before you decide a foreclosure is worth pursuing.

Identifying Properties Where Foreclosure Is More Likely

If your goal is property acquisition rather than interest income, you need to think strategically about which liens you are purchasing. Not every delinquent property is a realistic foreclosure candidate, and chasing the wrong ones wastes time and money.

Properties more likely to go through foreclosure without redemption tend to share certain characteristics. Absentee owners who have abandoned the property or lost interest in it are less motivated to redeem. Vacant lots with no improvements generate no income for the owner and offer little incentive to pay. Properties with no mortgage are not subject to lender pressure to cure the delinquency, which removes one of the most common forces that drives redemption.

On the other side, owner-occupied properties with active mortgages are among the least likely to result in foreclosure. The owner has somewhere to live and the lender has a financial stake in keeping the title clean. Both parties are motivated to resolve the lien before it goes further.

This does not mean you should only buy liens on abandoned properties. The underlying property value still matters enormously. A vacant lot in a depressed market that nobody wants is not a prize, even if you foreclose successfully. A vacant property in a growing area with strong resale demand is a completely different scenario.

Match your strategy to your goal. If you want interest income, focus on liens backed by solid properties with motivated owners. If you want the property, focus on liens where the owner appears disengaged and the property has real market value. Both strategies are valid. They just require different filters at the research stage.

The Due Diligence Required Before Pursuing Foreclosure

Before you initiate foreclosure, run a fresh round of due diligence on the property. Circumstances can change during the redemption period. A property that looked solid when you purchased the lien may have been damaged, vandalized, or further encumbered in the months since. Confirm that the math still works before you spend money on legal fees.

Your pre-foreclosure review should cover:

Current property condition. Use every available resource to assess the physical state of the property. If you can access it safely or hire someone to inspect it, do so. You need to know what you are actually acquiring before you invest additional money in the foreclosure process.

Updated title search. Pull a current title report to confirm that no new liens or encumbrances have appeared since your original purchase. Federal tax liens in particular can appear at any time and may affect your position in ways that complicate the foreclosure or reduce the value of what you end up owning.

Current market valuation. Real estate markets move. A property that was worth $180,000 when you bought the lien may be worth more or less today. Confirm that the current market value still justifies the foreclosure investment before you proceed.

Foreclosure cost estimate. Get a clear picture of what the legal process will cost you in your specific jurisdiction. Attorney fees, court filing costs, title work, and service of process expenses add up. A lien that looked profitable on paper can become marginal or worse once full foreclosure costs are factored in.

What You Actually Own After Foreclosure

If foreclosure completes successfully and you take title to the property, you own it the same way you would own any other piece of real estate, with one important caveat. In most states, a tax lien foreclosure extinguishes junior liens and other encumbrances, giving you a relatively clean title. However, certain obligations survive. Federal tax liens require special handling. Environmental liabilities attached to the land do not disappear because of a foreclosure. Code violations and municipal citations often transfer with ownership.

This is why a thorough title review before and after foreclosure is essential, not optional. You want to know exactly what you are taking on before you complete the process, not after.

Once you have clear title, your options are the same as any property owner. You can sell, rent, renovate, or hold depending on your strategy and the market conditions at the time. The acquisition cost, which is the lien amount plus foreclosure expenses, is almost always well below market value for properties where the process goes smoothly. That spread between your cost and market value is the equity position that makes this strategy attractive for investors targeting property ownership.

Managing Expectations for the Full Process

The realistic timeline from purchasing a lien certificate to acquiring a property, if that is even the outcome, runs anywhere from one to four years depending on the state's redemption period, how quickly the foreclosure process moves, and whether the action is contested. It is not a fast strategy for acquiring real estate.

What it is, for the right investor with the right property and the right market, is a disciplined path to acquiring real estate at a substantial discount to market value with a legally secured claim backing every step of the process. The investors who succeed with this approach are not the ones who stumbled into a foreclosure. They are the ones who identified the right property, understood the process, managed the timeline, and executed without cutting corners.

The process rewards preparation. It penalizes impatience.

Tax Lien Certificates vs. Tax Deeds: Understanding the Difference

If you are researching delinquent property tax investing, you will encounter two distinct strategies: tax lien certificates and tax deeds. Both are rooted in the same problem, a property owner who has stopped paying taxes, but they represent fundamentally different types of investments with different risk profiles, capital requirements, timelines, and outcomes. Choosing between them is not a matter of one being better than the other. It is a matter of which one fits your goals, your resources, and your appetite for complexity.

The Core Distinction

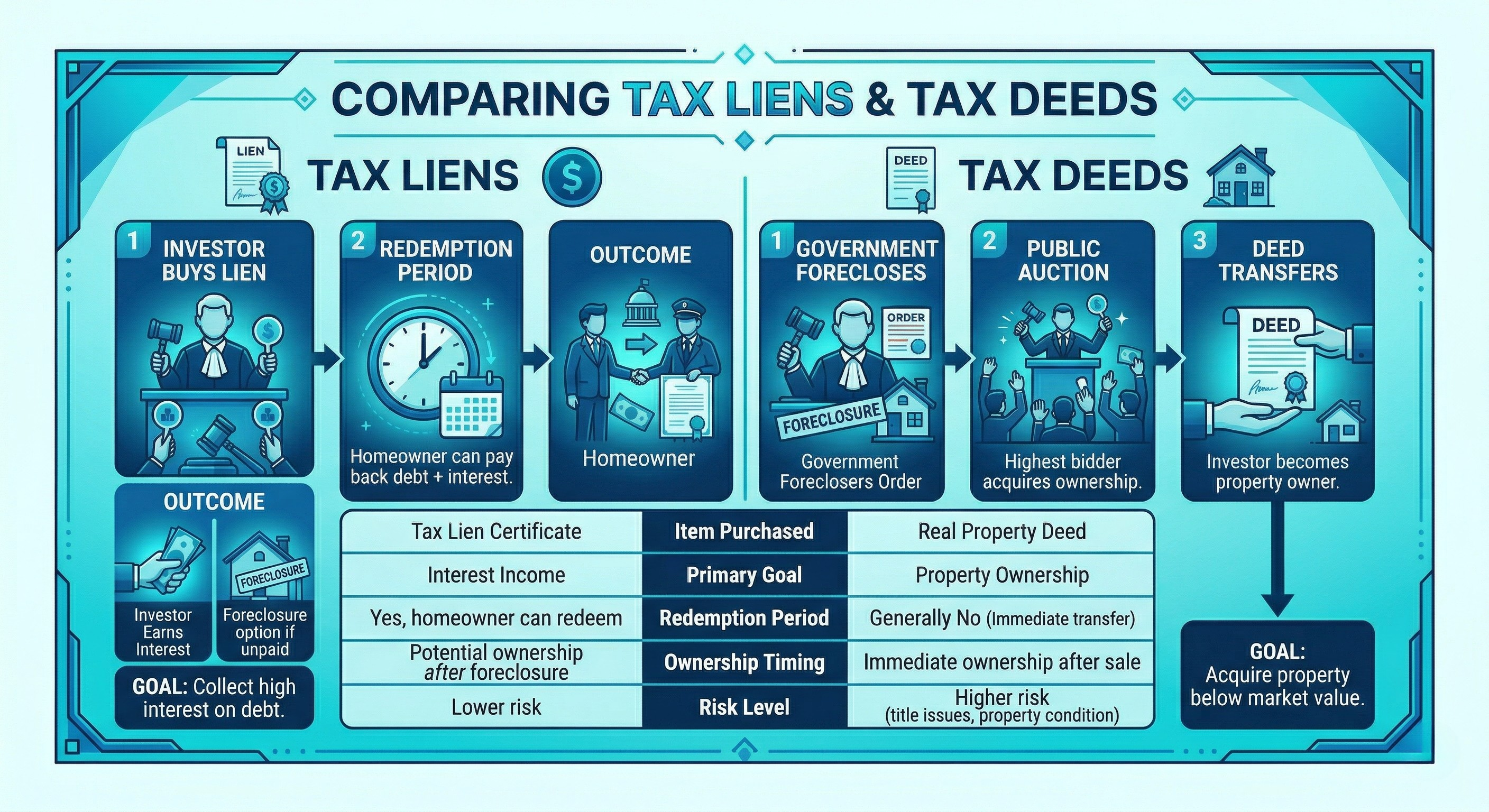

A tax lien certificate is a debt instrument. When you purchase one, you are paying the delinquent tax balance on behalf of the property owner and stepping into the government's position as the lienholder. You do not own the property. You own a legal claim against it, secured by the real estate, that earns interest at a rate set by state law. Your most likely outcome is that the owner repays the debt with interest during the redemption period and you collect your return without ever touching the property.

A tax deed is a direct property conveyance. In tax deed states, the government skips the lien stage entirely, or completes it internally, and sells the property itself at public auction after taxes have gone unpaid long enough to trigger the deed process. When you win a tax deed auction, you are purchasing ownership of the property, not a claim against it. You leave the auction as the new owner, or close to it depending on the state's process.

That distinction, debt versus ownership, drives every other difference between the two strategies.

Tax Lien Investing: What You Are Actually Signing Up For

Tax lien investing is primarily an income strategy. Your return comes from interest payments, not from property appreciation or rental income. Because most property owners redeem their liens before losing their homes, the typical investor experience is: purchase certificate, wait through redemption period, collect principal plus interest. The property serves as collateral that secures your position, not as an asset you plan to manage or sell.

This structure makes tax lien investing relatively predictable compared to direct real estate investment. You know the interest rate before you bid. You know the redemption period. You know the legal framework that governs your rights. What you cannot fully control is whether the underlying property holds its value as collateral in the event the owner does not pay, which is why property research before bidding is essential regardless of how "passive" the strategy appears.

The capital requirements for tax lien investing are also generally lower than tax deed investing. Individual certificates can be purchased for hundreds or thousands of dollars rather than the tens of thousands typically required to compete at a tax deed auction. This makes tax lien investing more accessible to investors who are building their portfolio incrementally.

The tradeoff is time. Redemption periods can stretch from six months to three years depending on the state. Your capital is tied up for that duration, and you have limited ability to accelerate the timeline. Investors who need liquidity or faster capital turns may find tax deed investing more aligned with their needs despite the higher complexity.

Tax Deed Investing: What Changes When You Are Buying the Property

In a tax deed state, the government has already completed its internal process of attempting to collect unpaid taxes and has determined that the property will be sold to recover the debt. The auction you participate in is selling the property itself, and the winning bidder typically receives a tax deed conveying ownership, sometimes immediately and sometimes after a short post-auction redemption window depending on the jurisdiction.

The immediate upside is obvious. You acquire real property, often at a price below market value because distressed asset auctions attract different dynamics than traditional real estate sales. If you buy well and the property is in reasonable condition with a clean enough title, you can generate significant equity from the moment you take ownership.

The complexity, however, is substantially higher than lien investing. Several factors demand careful attention:

Title quality is the most significant concern. Tax deeds do not always convey clean title. Depending on the state, certain liens may survive the tax deed process. Federal tax liens, for example, are not automatically extinguished and can remain attached to the property after you take ownership. Mechanic's liens, environmental claims, and other encumbrances can also create complications. Before bidding at a tax deed auction, you need a title search and a clear understanding of what survives the sale in that specific jurisdiction. Purchasing title insurance immediately after acquisition is standard practice for sophisticated tax deed investors, and you should budget for it.

Property condition is entirely your risk. Unlike a traditional real estate purchase, tax deed acquisitions typically come with no seller disclosures, no inspection contingencies, and no recourse if you discover problems after the fact. You are buying the property as-is, sight often unseen, which means your pre-auction due diligence on the physical condition of the property is doing the work that an inspection would do in a normal transaction. Drive the property, pull permit records, check for code violations, and look for any signs of environmental issues before you bid.

Capital requirements are higher and less flexible. Tax deed auctions often require immediate payment in full, or payment within 24 to 48 hours of winning. The purchase prices, while below market, are still real estate prices. You need sufficient capital not just to win the auction but to cover title work, any necessary repairs, holding costs, and the carrying expenses while you decide what to do with the property.

Post-acquisition strategy must be planned in advance. When you win a tax deed auction, you own real estate. That means you need a plan. Are you flipping it? Holding it as a rental? Selling it to another investor? Each path has its own requirements, timeline, and cost structure. Investors who win a tax deed without a clear exit strategy often find themselves holding an asset that costs money every month while they figure out what to do with it.

How States Are Structured: Lien States, Deed States, and Hybrid Systems

The strategy available to you depends heavily on where you are investing. States generally fall into one of three categories:

Tax lien states sell lien certificates to investors and give property owners a redemption period before foreclosure can begin. Florida, Arizona, New Jersey, Illinois, and Colorado are among the most active tax lien states, each with their own interest rate structures and auction formats.

Tax deed states skip the certificate stage and sell the property directly after the tax delinquency reaches a trigger point. Georgia, California, Michigan, and Texas operate primarily as tax deed states, though the specifics of each state's process differ considerably.

Hybrid states use elements of both systems. Some sell liens but also conduct deed sales for properties that go unredeemed over multiple cycles. Others have county-by-county variation in how they handle delinquent tax properties. Researching the specific rules of the state and county you are targeting is not optional. The rules governing your rights, your timeline, and your obligations all flow from that framework.

Over-the-Counter Properties: The Overlooked Opportunity

In both lien and deed states, not every property sells at auction. When a tax lien certificate or tax deed property fails to attract a winning bid during the public auction, it does not disappear. In many jurisdictions, it becomes available for purchase directly from the county through what is called an over-the-counter sale, commonly referred to as OTC.

OTC properties can be purchased at a fixed price, typically the minimum bid that went unclaimed at auction, without competing against other bidders. For investors who find auctions stressful, who want more time to research before committing, or who are looking for ways to deploy capital outside of auction cycles, OTC inventories can be a productive source of deals.

But the reason these properties went unsold at auction matters enormously, and it is the first question any serious OTC investor should ask. Properties end up in OTC inventory for a variety of reasons. Some were simply overlooked in a large auction with dozens or hundreds of listings. Others were passed over by experienced investors who found something during their research that made the property unattractive. The difference between those two scenarios is everything.

Common reasons experienced investors pass on properties at auction, and why they show up in OTC inventory, include:

Location issues. The property may be in an area with declining values, limited buyer demand, or proximity to industrial sites, flood zones, or other factors that suppress marketability.

Title complications. Serious title defects, surviving federal liens, or legal clouds on the ownership history may have made the property unbiddable for anyone who did their homework.

Physical condition. Structural damage, fire damage, environmental contamination, or condemnation status can render a property more liability than asset.

Size or type issues. Vacant lots with no development potential, landlocked parcels with no legal access, or fractional interests in properties can be difficult or impossible to monetize.

None of this means OTC properties are categorically bad investments. Overlooked properties in strong markets, or properties passed on due to manageable issues that you are equipped to resolve, can represent genuine opportunity. The OTC channel is also less competitive than live auctions, which gives you more time to research and more leverage in evaluating whether a deal actually works.

The discipline required for OTC investing is the same discipline required everywhere in this asset class: research the property thoroughly, understand why it did not sell, confirm that the reason is not a dealbreaker for your specific situation, and make sure the numbers work even after you account for every cost you are likely to encounter.

Choosing Between Liens and Deeds: A Framework for Deciding

The right strategy depends on what you are trying to accomplish and what you are prepared to handle.

Tax lien investing is better suited for investors who want predictable, interest-based returns without taking on property management responsibilities, who are building a portfolio incrementally with moderate capital, who prefer a more defined legal framework with clearer timelines and outcomes, and who are comfortable with capital being tied up through a redemption period.

Tax deed investing is better suited for investors who are comfortable with real estate ownership and the responsibilities it carries, who have sufficient capital to handle acquisition costs plus the unexpected expenses that come with distressed properties, who have a clear exit strategy for any property they acquire, and who are willing to do deep due diligence on physical condition and title before bidding on anything.

Neither strategy is beginner-proof. Both reward preparation and punish shortcuts. But understanding which one aligns with your current resources, goals, and risk tolerance is the foundational decision that determines everything that comes after it.

Tax Lien Investing Strategy and Methods

Most investors who struggle with tax lien investing do not struggle because the strategy is too complicated. They struggle because they never developed a strategy in the first place. They show up to auctions, buy whatever looks interesting, and then wonder why results are inconsistent. The investors who build reliable returns in this space operate from a defined methodology that governs which markets they target, which liens they buy, how they size their positions, and how they manage their portfolio over time. That is what this section is about.

Start With a Clear Investment Objective

Before you develop any strategy, you need to know what you are trying to accomplish. Tax lien investing can serve very different goals depending on how it is structured, and the approach that works for one objective will underperform for another.

If your primary goal is interest income, your strategy centers on acquiring liens with strong redemption likelihood, favorable interest rates, and solid underlying collateral. You want your money returned with interest, reliably and repeatedly, without having to pursue foreclosure. Your filters at the research stage prioritize owner-occupied properties, active mortgages on the property, strong neighborhood demand, and states with high statutory interest rates.

If your primary goal is property acquisition, your strategy looks completely different. You are deliberately targeting liens on properties where redemption is less likely, where the owner appears disengaged, and where the underlying property has genuine market value if you end up taking title through foreclosure. You are willing to wait longer, spend more on legal fees, and manage a more complex process in exchange for the potential to acquire real estate at a significant discount.

Most investors start with the income objective and develop the expertise to pursue selective property acquisition over time. Trying to do both simultaneously without a clear framework leads to a portfolio that is unfocused and harder to manage.

The Tax Yield Strategy: Maximizing Interest Income

Tax yield investing is the most straightforward application of the lien certificate model. The goal is simple: acquire liens that will be redeemed, earn the statutory interest rate, and redeploy that capital into the next round of certificates. Executed consistently across a diversified portfolio, this approach can generate predictable, compounding returns backed by real estate collateral.

The key to making this strategy work is understanding where the best yield opportunities actually exist and how to screen for them systematically.

Interest rates vary dramatically by state. New Jersey historically offers rates up to 18%. Illinois certificates can earn up to 36% on a penalty basis depending on the structure. Florida starts at 18% but gets bid down aggressively in competitive counties. Arizona offers up to 16%. Iowa has a fixed rate structure that removes the bid-down dynamic entirely, which some investors prefer for its predictability. Knowing the rate environment in your target state before you commit to it is foundational.

But the highest stated rate is not always the best yield. In states where investors bid down the interest rate, competitive urban counties often see rates pushed to near zero on desirable properties. The headline rate of 36% in Illinois means very little if you are bidding in Cook County and the competitive pressure drives your actual rate to 2% or 3%. Yield-focused investors frequently target less competitive rural counties within high-rate states, accepting slightly more research complexity in exchange for rates that actually reflect the statutory maximum or close to it.

Strong redemption likelihood is the other half of the yield equation. A lien that earns 24% annually but never gets redeemed is not a yield investment, it is a foreclosure situation you did not plan for. Screening for high redemption likelihood means focusing on properties with active mortgages, where the lender has a financial incentive to ensure the lien is resolved. It means prioritizing owner-occupied residential properties where the owner has a personal stake in retaining the home. It means avoiding vacant lots, abandoned structures, and properties in markets with declining demand, all of which carry higher non-redemption risk.

Geographic Diversification: How to Think About Market Selection

Concentrating your entire portfolio in a single county or state creates exposure to local economic conditions, policy changes, and competitive dynamics that can affect your returns across the board. A county that changes its auction format, a state legislature that adjusts statutory interest rates, or a local real estate downturn can impact every certificate in a geographically concentrated portfolio simultaneously.

Diversifying across multiple states and counties is the standard risk management approach for serious tax lien investors. But diversification for its own sake is not a strategy. It needs to be structured around a clear understanding of each market you are entering.

When evaluating a new state or county, the questions that matter most are: What is the statutory interest rate and how aggressively does it get bid down in this market? What is the redemption period and does it fit my capital timeline? What is the foreclosure process and how long does it take if I need to use it? How are auctions conducted, online or in person, and what are the registration and funding requirements? What is the quality and accessibility of the county's public records and auction lists?

Some investors build a tiered geographic structure. A core set of two or three well-understood markets where they invest consistently, and a secondary tier of markets they are actively researching and testing with smaller positions. This approach balances the efficiency of deep market knowledge with the risk management benefits of not being entirely dependent on a single jurisdiction.

Building a Tax Lien Portfolio: Position Sizing and Structure

A single tax lien certificate is not a portfolio. It is a single bet on a single property in a single jurisdiction. The goal of portfolio building is to spread risk across enough positions that the performance of any individual certificate does not determine your overall outcome.

For most investors starting out, the practical question is how to build toward a diversified portfolio when capital is limited. The answer is to start with smaller certificates across several properties rather than concentrating available capital in one or two larger liens. A portfolio of ten $1,000 certificates in different properties across two or three counties is structurally more resilient than a single $10,000 certificate, even if the individual research quality is identical.

As the portfolio grows, position sizing should reflect the risk profile of each certificate. A lien on an owner-occupied property in a stable neighborhood with a strong assessed value can reasonably represent a larger position. A lien on a property with higher non-redemption risk, where you may end up pursuing foreclosure, should represent a smaller position sized to account for the additional time, legal costs, and uncertainty involved.

Tracking your portfolio requires real infrastructure, not a mental note. Every certificate should be documented with the property address, lien amount, interest rate, purchase date, redemption deadline, required notice dates, and current status. A simple spreadsheet works at the start. As the portfolio scales, purpose-built tracking tools or real estate investment software become worth the investment. Missing a redemption deadline or a required notice date because your record-keeping broke down is an expensive and entirely preventable mistake.

Reinvestment and Compounding: How the Strategy Builds Over Time

The mathematical engine behind a well-run tax lien portfolio is reinvestment. When a certificate redeems and you collect your principal plus interest, deploying that capital immediately into the next round of certificates is what drives compounding returns over time.

This sounds obvious, but many investors leave redeemed capital sitting idle between auction cycles because they have not planned their reinvestment cadence. Auction schedules vary by county and many run only once or twice a year. Knowing when your target counties hold auctions and planning your capital availability around those dates is part of operating the strategy efficiently.

Investors who run this system well over several years often find themselves with a self-funding acquisition machine. Returns from redeemed certificates fund the next round of purchases. The portfolio grows without requiring constant capital infusions from outside the strategy. That compounding effect, applied consistently across a diversified set of certificates in favorable markets, is what makes the tax yield approach genuinely interesting as a long-term income strategy.

What "Passive" Actually Looks Like in Practice

Tax lien investing is frequently described as passive income, and relative to operating a rental property, it is. There are no tenants, no maintenance calls, no property management decisions, and no physical asset to oversee on a daily basis. But passive does not mean unattended.

A functioning tax lien operation requires consistent attention to several things. Redemption deadlines must be tracked and calendared for every certificate in the portfolio. Required notices to property owners must be sent on time and documented. Auction calendars across your target markets need to be monitored so you are prepared to deploy capital when opportunities arise. New certificates need to be researched before each auction cycle. And the overall portfolio needs periodic review to assess performance, identify any certificates approaching foreclosure decisions, and reallocate capital from redeemed positions.

For an investor managing a modest portfolio of ten to twenty certificates, this might represent a few hours of work per month. For an investor managing a hundred or more certificates across multiple states, it becomes a more substantial operational commitment that may warrant dedicated administrative support or software infrastructure.

The point is not that tax lien investing is high-maintenance. It is that the investors who treat it as something that runs itself without attention are the same investors who miss deadlines, lose rights, and wonder why their results do not match the promise. The ones who build real systems around it, even simple ones, consistently outperform.

The strategy is sound. The execution is what you control.

Tax Lien Investing Returns and Interest Rates

Returns in tax lien investing are real, but they are also more nuanced than the headline numbers suggest. Understanding what drives your actual yield, not just the stated rate, is what separates investors who build consistent returns from those who are perpetually disappointed by results that do not match expectations.

How Interest Rates Are Set

Every state that operates a tax lien system establishes a maximum allowable interest rate by statute. This is the rate the property owner must pay when redeeming the lien, and it is the foundation of your return as the investor. These rates vary significantly from state to state and represent one of the primary factors in evaluating which markets to target.

To give you a concrete picture of the landscape:

Florida sets its maximum rate at 18% annually, with a minimum rate floor of 5% even if bidding pushes lower. New Jersey allows rates up to 18%. Arizona caps rates at 16%. Illinois operates on a penalty-based system that can effectively translate to returns of 24% to 36% depending on the redemption timing. Iowa uses a fixed monthly rate system that currently translates to roughly 24% annually without the bid-down dynamic. Colorado allows rates up to 15%. Indiana operates on a system with rates up to 25%.

These are not guaranteed returns. They are the maximum rates available before auction competition and redemption timing affect your actual yield. But they illustrate why tax lien certificates consistently attract attention from income-focused investors. Fixed income alternatives like Treasury bonds, CDs, and money market accounts rarely approach these figures, and tax liens carry real collateral in the form of real property behind every certificate.

How Auction Competition Affects Your Real Yield

The stated statutory rate and the rate you actually earn are often two different numbers, and understanding why is critical before you enter any market.

In bid-down states, investors compete by accepting lower interest rates rather than by paying higher prices. The auction starts at the maximum statutory rate and investors bid the rate downward until no one will go lower. The investor willing to accept the lowest rate wins the certificate.

Here is what that looks like in practice. You are bidding in a Florida county on a lien with a statutory maximum of 18%. The property is a well-maintained single-family home in a desirable neighborhood with an active mortgage. Experienced investors in the room know this lien will almost certainly redeem. The bidding starts at 18% and drops quickly. By the time the gavel falls, the winning rate might be 5%, 3%, or even 0.25%. The winner technically holds a lien, but the return on that specific certificate is a fraction of what the headline rate implied.

This dynamic is most pronounced in densely populated counties with competitive investor pools and properties with obvious appeal. It is considerably less intense in rural counties, smaller markets, and properties that require more research effort to evaluate. Many experienced investors deliberately avoid the most competitive urban markets in high-rate states and instead focus on mid-size or rural counties within those same states where bid-down pressure is lower and rates closer to the statutory maximum are achievable.

In premium bid states, the rate is fixed and investors compete by paying a premium above the lien amount. The mechanics are different but the yield compression effect is similar. You might pay $5,800 for a $5,000 lien in a competitive auction. The property owner redeems by paying $5,000 plus the fixed interest rate, not your $5,800. The $800 premium you paid is your loss, and it reduces your effective yield accordingly. Calculating your real return in a premium bid environment requires you to factor that premium into your cost basis before you ever place a bid.

How Redemption Timing Affects Annualized Returns

The interest rate on a tax lien certificate is typically expressed as an annual figure, but most liens do not run for exactly one year. Redemption timing directly affects your annualized return in ways that are not always intuitive.

Consider a certificate with a 24% annual interest rate and a lien amount of $3,000. If the owner redeems at exactly 12 months, you collect $3,000 plus $720 in interest for a total of $3,720. Straightforward.

But if the owner redeems at three months, you collect $3,000 plus $180 in interest, your capital is returned in 90 days, and your annualized return on that deployment is still 24% because the rate accrues proportionally. That is actually a favorable outcome because your capital is freed up to be redeployed into the next certificate sooner.

Where redemption timing works against you is in states with minimum interest provisions. Florida, for example, mandates a minimum interest payment equivalent to 5% of the lien amount regardless of how quickly the owner redeems. If an owner redeems a Florida lien after just two weeks, you collect the 5% minimum rather than the prorated 18% annual rate, which translates to an annualized return well above the stated maximum. That sounds positive, but it also means your capital cycled out in two weeks and must now be redeployed, introducing reinvestment timing into your return calculation.

In states without minimum interest provisions, very early redemptions can produce lower absolute dollar returns than you projected. The annualized rate still looks strong, but the actual dollars collected on a short-duration redemption can be modest. Managing a portfolio of certificates across varying redemption timelines requires you to think about capital deployment and reinvestment cadence, not just individual certificate rates.

Penalty-Based Systems Versus Straight Interest Systems

Not all states calculate returns using a simple annual interest rate. Some use penalty-based structures that work differently and can produce higher effective returns depending on redemption timing.

Illinois is the most prominent example. Rather than earning a straight annual interest rate, Illinois tax lien investors earn a penalty that accrues in six-month intervals. The penalty rate is set at each auction and can reach up to 18% per six-month period, which translates to a potential annualized return of 36% if the lien redeems after six months or more. However, if the lien redeems before six months, the investor earns the full six-month penalty anyway, which means very early redemptions produce returns that exceed 36% on an annualized basis.

This structure creates a different return profile than a straight interest state and attracts a specific type of investor strategy. Understanding whether your target state uses straight interest, penalty-based accrual, a fixed monthly rate, or some hybrid is foundational research before you commit capital to any market.

What Realistic Returns Actually Look Like

With all of those variables in play, what should a serious tax lien investor actually expect to earn?

The honest answer depends heavily on market selection, auction discipline, and portfolio management quality. Investors operating in competitive urban markets in bid-down states and paying premiums for the most desirable certificates may find their effective yields in the 3% to 8% range after accounting for bid-down compression and reinvestment timing. That is still competitive with many fixed income alternatives, particularly given the collateral backing, but it is far from the 24% or 36% headline rates that attract attention.

Investors who target less competitive markets, maintain bidding discipline, focus on mid-range lien amounts that institutional investors often overlook, and reinvest capital consistently across multiple auction cycles can realistically target effective yields in the 10% to 18% range in favorable states. Investors who add selective foreclosure opportunities to their income-focused strategy, acquiring undervalued properties on liens that do not redeem, can generate returns that are harder to quantify in percentage terms but represent significant equity creation.

The range of outcomes is wide, and that width reflects the degree to which this strategy rewards active management. Passive participation in tax lien auctions without research or strategy produces mediocre results. Disciplined, systematic participation in carefully selected markets produces something meaningfully different.

The Real Risks of Tax Lien Investing (And How to Think About Each One)

Every investment carries risk. What separates informed investors from uninformed ones is not the absence of risk but the ability to identify it clearly, understand its implications, and make deliberate decisions about how much of it to accept and under what conditions. Tax lien investing has a specific and learnable risk profile. None of the risks covered in this section should discourage a prepared investor. All of them should disqualify an unprepared one.

Property Value Risk

This is the foundational risk in tax lien investing and the one that causes the most damage to investors who skip their research. When you purchase a tax lien certificate, the property behind it is your collateral. If that property has no meaningful market value, your collateral is worthless regardless of what the lien says on paper.

The scenario plays out like this: you purchase a lien on a property that looks acceptable based on the county assessment records. The owner does not redeem. You initiate foreclosure and eventually take title. Then you discover the property is a condemned structure, or a landlocked parcel with no legal road access, or a lot in a market where nothing has sold in three years. The lien amount you paid is gone, you have incurred legal fees on top of it, and you now own an asset that costs money to hold and cannot be easily sold.

This outcome is entirely preventable with proper research before bidding. County assessed values are a starting point, not a final answer, and they frequently lag real market conditions by years. Before purchasing any certificate, verify the current market value using comparable sales data, not just the assessment. Research the neighborhood trajectory. If the property is local, drive by it. If it is not, use every available remote resource to understand what you would actually be acquiring in a foreclosure scenario.

The rule is simple: never purchase a lien on a property you would not be comfortable owning at the price you paid for the certificate plus your foreclosure costs.

Title Risk

Title complications are among the most technically complex risks in tax lien investing and among the most expensive when they surface after you have already committed capital.

The specific risks depend heavily on the state you are operating in and the type of lien or deed you are acquiring. The most important categories to understand are:

Federal tax liens. The IRS has special status under federal law. In many states, a federal tax lien does not get extinguished by a tax lien foreclosure the way junior liens do. This means you can complete the entire foreclosure process, take title to a property, and still have an IRS lien attached to it that must be resolved before you can sell with clean title. Federal liens have their own redemption rights and their own timeline that operates separately from the state process. Always check for IRS liens before bidding on any certificate.

Surviving encumbrances. Depending on the state, certain other obligations can survive a tax lien foreclosure. Environmental liabilities attached to contaminated land do not disappear because of a change in ownership. Municipal code violations, unpaid utility liens in some jurisdictions, and homeowner association assessments in certain states can transfer with the property. Each of these represents a cost you did not plan for.

Unclear ownership history. Properties with fractional interests, disputed inheritance, or unresolved estate issues can create title clouds that make foreclosure complicated and the resulting title difficult to insure or sell. A thorough title search before purchase is the only way to identify these issues in advance.

Title insurance. For any property you acquire through foreclosure, purchasing title insurance immediately after taking ownership is standard practice among experienced investors. It is not an optional expense. It is the mechanism that protects your position if a title defect surfaces after the fact. Budget for it as part of your foreclosure cost calculation.

Redemption Period and Liquidity Risk

Tax lien certificates are illiquid investments. Once you purchase one, your capital is committed until the lien resolves, either through redemption or foreclosure. You cannot call the county and ask for your money back if you need capital for something else. You generally cannot sell the certificate on a secondary market with any speed or predictability, though some states do allow lien transfers. Plan accordingly.

The redemption period extends this illiquidity for a defined but sometimes lengthy timeline. In states with two or three year redemption periods, capital deployed at one auction may not be returned until well into the following years. For investors with tight capital constraints or a need for predictable liquidity, this timeline creates real planning challenges.

The practical implication is that you should never invest capital in tax lien certificates that you cannot genuinely afford to have tied up through the full redemption period plus whatever time a foreclosure process might require if it comes to that. A worst-case timeline in a state with a two-year redemption period and a complex foreclosure process could keep your capital committed for three to four years on a single certificate. Size your positions accordingly and maintain sufficient liquid reserves outside your lien portfolio.

Legal and Compliance Risk

This is the risk that blindsides new investors most often because it does not feel like an investment risk. It feels like paperwork. But failing to comply with the legal requirements governing your lien can invalidate rights you paid for and cannot recover.

Most states require investors to send formal notice to property owners at specific points during the redemption period and before initiating foreclosure. These notice requirements have precise specifications: what the notice must say, how it must be delivered, to whom it must be sent, and by what deadline. Missing a required notice, sending it in the wrong format, or serving it to the wrong address can legally extinguish your right to foreclose even if the owner never paid a single dollar.

Some states require you to pay subsequent year taxes on a property to maintain your lien position. If a second or third year of taxes becomes delinquent and you do not pay them, another investor can purchase a subsequent lien that may affect your position depending on state law.

The foreclosure process itself has filing deadlines, service of process requirements, and court procedures that vary by jurisdiction. Errors at any stage can require refiling, extend your timeline significantly, or in some cases require starting over entirely.

None of this is unmanageable. But it requires you to know the rules of the specific state you are operating in before you are in the middle of a situation where the rules matter. Work with a local attorney who understands tax lien law in your target state before you face a foreclosure situation for the first time, not after.

Environmental Risk

Environmental contamination is a low-probability but high-consequence risk that deserves specific attention for investors considering properties that might go to foreclosure. If you take title to a property through foreclosure and that property has environmental contamination, you may inherit the cleanup liability as the new owner. Environmental remediation costs can run from tens of thousands to millions of dollars depending on the nature and extent of the contamination.

Properties most likely to carry environmental risk include former gas stations, dry cleaners, auto repair shops, agricultural land with chemical storage history, and any commercial or industrial property. Residential properties in neighborhoods near industrial sites also warrant attention.

For the vast majority of residential tax lien investing in established neighborhoods, environmental risk is not a significant concern. But for any property with commercial history, prior industrial use, or proximity to known contamination sites, a basic environmental assessment before pursuing foreclosure is a reasonable precautionary step. The cost of that assessment is trivial compared to the cost of discovering contamination after you own the property.

Auction and Overbidding Risk

Auctions create psychological pressure that can override rational analysis if you are not disciplined going in. This is not a character flaw. It is a well-documented behavioral pattern that affects experienced investors as well as beginners. The competitive environment of an auction, whether in a county courthouse or on a digital platform, creates momentum that pushes people to bid beyond the point where the math still works.

In bid-down states, overbidding means accepting a lower interest rate than your target. If you set a minimum acceptable rate of 8% before the auction and then watch yourself bid down to 3% because you got caught up in the competition, you have not made a disciplined investment. You have made an emotional one.

In premium bid states, overbidding means paying more above the lien amount than your return justifies. The math here is unforgiving. Run the numbers before you bid and know your maximum premium before the auction starts, not in the moment.

The discipline to walk away from a certificate where the economics no longer work, even after you have spent hours researching the property, is one of the most important skills in tax lien investing. The research you did on a deal you did not buy is not wasted. It is practice that makes your next auction more efficient.

Market and Concentration Risk

Concentrating your portfolio in a single county, state, or property type creates exposure to local conditions that can affect multiple certificates simultaneously. A regional economic downturn, a major employer leaving a market, a natural disaster, or a state legislative change to the tax lien statute can all affect your portfolio in ways that geographic concentration amplifies.

Diversification across states and counties reduces this exposure. So does diversifying across property types, mixing residential with commercial where your expertise supports it, and varying the lien amounts and redemption timelines within your portfolio.

Concentration risk also applies to auction strategy. Investors who buy exclusively in one county's annual auction have their entire portfolio correlated to that single market's conditions and auction dynamics. Building a pipeline across multiple markets and auction cycles creates a more resilient deployment pattern.

Common Mistakes That Create Unnecessary Risk

Beyond the structural risks above, most underperformance in tax lien investing traces back to a handful of specific execution mistakes. Understanding them in advance is the most direct path to avoiding them.

Buying without physically or remotely assessing the property. Assessment records, aerial imagery, and tax maps are starting points. They are not substitutes for understanding what a property actually looks like and what condition it is in. Investors who bid on properties they have never evaluated visually are accepting risk they cannot quantify.

Treating the stated interest rate as the expected return. As covered in the returns section, competition, bid-down dynamics, redemption timing, and premium costs all affect what you actually earn. Investors who enter markets assuming they will earn the statutory maximum without accounting for these factors consistently overestimate their returns before the fact and are disappointed by them after.

Failing to track subsequent tax obligations. In states where subsequent year taxes affect your lien position, ignoring annual tax bills on properties in your portfolio is a real and avoidable mistake. Build a system that flags upcoming tax due dates on every property behind a certificate you hold.