How to Buy Property with Delinquent Taxes: A Practical Guide

Plenty of investors have heard that you can buy property through delinquent tax sales for a fraction of its market value. Fewer actually understand what that process looks like — or what can go wrong when you skip the steps.

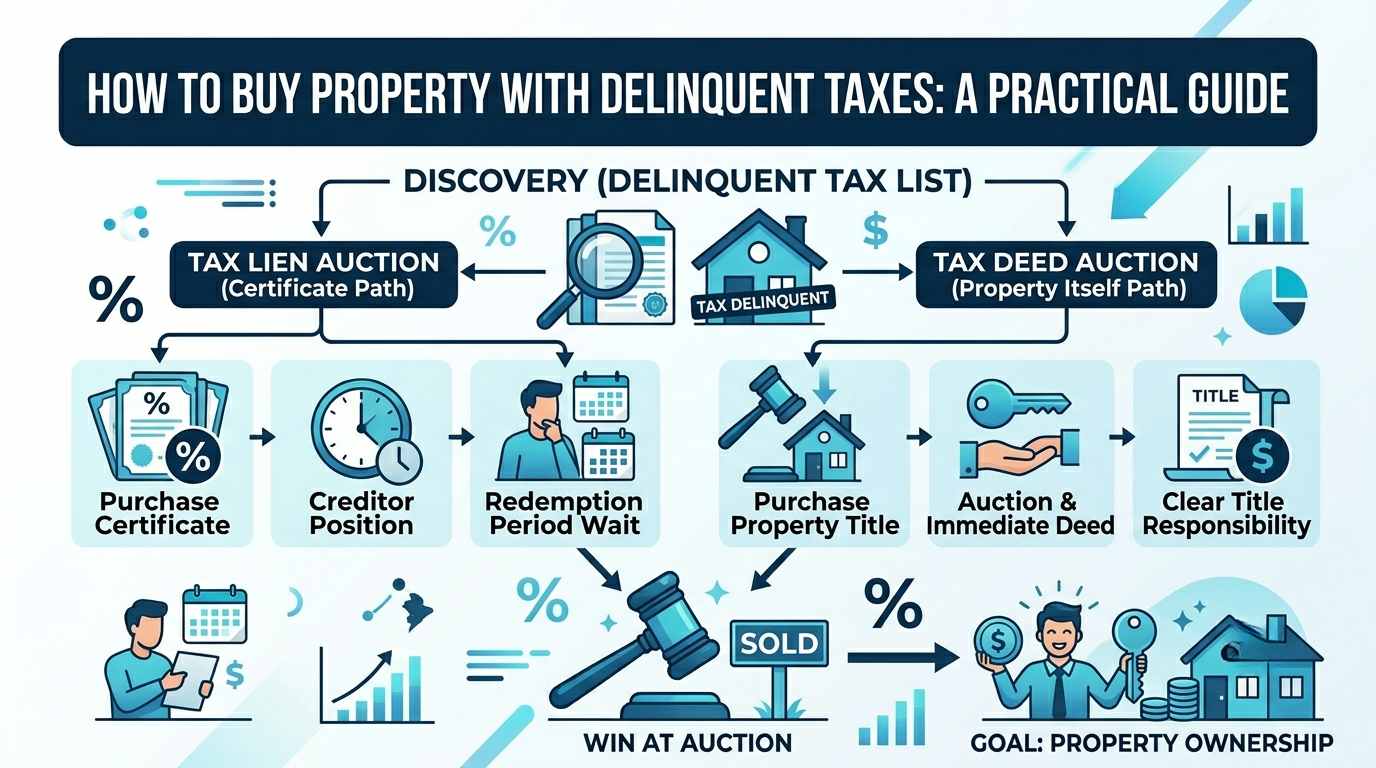

Buying property connected to delinquent property taxes is real and legal. Governments need to recover unpaid taxes, and the mechanism for doing that creates legitimate investment opportunities. The path to those opportunities runs through two different systems — tax lien auctions and tax deed auctions — and the rules, risks, and returns are different in each.

This guide covers both. By the end, you will know what 'delinquent tax property' actually means in legal terms, how to navigate each type of sale, and what to do after you win at auction.

New to Tax Lien Investing? Before diving into the buying process, get the full picture on how tax lien and tax deed strategies work — start with the foundations. → Read: Tax Lien vs. Tax Deed — Key Differences Every Investor Must Know |

What Does 'Buying Property with Delinquent Taxes' Actually Mean?

When a property owner stops paying their property taxes, the local government does not immediately seize the property. Instead, it typically waits through a delinquency period — often one to three years — during which interest and penalties accumulate on the unpaid balance.

After that window closes, the government takes action to recover the debt. That action takes one of two forms depending on the state: selling a tax lien certificate to investors (in tax lien states) or seizing the property and selling it directly (in tax deed states). Either way, the result is a public auction where investors can acquire either the government's claim on the property or the property itself.

Neither system is a loophole. Both are established legal frameworks that governments use to enforce tax collection. The investor's role is to participate in the process that already exists — not to exploit property owners, but to provide liquidity to a system that needs it. For a more detailed explanation of how tax lien investing works as a complete investment strategy, see our overview.

Two Ways to Buy: Tax Liens vs. Tax Deeds

The strategy you follow depends entirely on which state — and which county — you are targeting. The rules are set at the state level. You do not choose between the two strategies; your target location determines which one is available to you.

Buying via Tax Lien Certificate

In a tax lien state, you do not buy the property at auction. You buy the government's right to collect the unpaid taxes — plus statutory interest — from the property owner. The certificate is a senior lien on the property, meaning it takes priority over most other claims.

The property owner then has a redemption period — legally defined by state statute — during which they can pay you the face amount of the lien plus all accrued interest. If they redeem, you earn your return and the transaction is complete. If they do not redeem by the deadline, you gain the right to initiate tax lien foreclosure proceedings, which can ultimately result in you taking ownership of the property.

The vast majority of tax lien certificates — typically 95% or more — are redeemed before foreclosure is necessary. The lien-to-property path is the exception, not the expectation.

Buying via Tax Deed Auction

In a tax deed state, the county forecloses on the property on behalf of the government and then auctions the property itself. When you win at a tax deed auction, you receive a deed — legal title to the property — at the close of the auction.

There is no redemption periodThe legally defined timeframe during which a property owner can reclaim their property by paying the delinquent taxes plus interest and penalties. after the sale (though the property owner had a pre-sale window to pay the back taxes). You own the property immediately and can begin taking action — resell it, rent it, rehab it — subject to any due diligence steps you should have completed before bidding.

Some states use a hybrid model called a redeemable tax deed, where you receive the deed at auction but the prior owner can still redeem within a defined window. Texas, Georgia, and Tennessee are the primary examples.

Step-by-Step: How to Buy Property Through a Delinquent Tax Sale

The process is the same whether you are buying a lien or a deed — up to a point. Here are the six steps that apply to both.

Step 1 — Identify Your State's Sale Type

Before anything else, confirm whether your target state operates as a tax lien state, tax deed state, or hybrid. This is not optional research — the entire process downstream depends on it. The county treasurer's or tax collector's website is the authoritative source. State classification databases from investment education resources are useful for orientation but always verify with the county directly.

Step 2 — Research the County Auction Schedule

Auctions are held at the county level on schedules set by county offices. Some counties auction monthly; others annually. Some have moved to online platforms like RealAuction or Bid4Assets; others remain in-person. Registration requirements, deposit amounts, and payment windows vary by county.

Key questions to answer before registering: When is the next auction? Is it online or in-person? What is the registration deadline? What deposit is required? What are the payment terms after winning? These details are available on the county tax collector's website or by calling the office directly.

Step 3 — Due Diligence on the Property

This is the most important step and the one most frequently underweighted by new investors. Every property you consider bidding on requires its own research. For tax lien certificates, the core question is whether the property's market value justifies the lien amount plus any estimated foreclosure costs. If the owner does not redeem and the property is worth less than what you paid, you face a loss.

For tax deed properties, the questions expand: What does the title look like? Are there surviving encumbrances (especially federal tax liens, which can survive a tax deed sale)? What is the physical condition? What will it take to make the property saleable? For a primer on how to evaluate the underlying real estate in both strategies, see how tax lien wealth builders works.

Due diligence sources for both: county assessor records (assessed valueThe dollar value assigned to a property by a local tax assessor for the purpose of calculating property taxes., ownership history), GIS maps (parcel boundaries, flood zone status), satellite imagery, and public court records (active bankruptcies, federal liens).

Step 4 — Register and Prepare Your Capital

Most county auctions require pre-registration and a deposit before you are permitted to bid. Arrive with this handled well in advance of the auction date. Many online auctions have registration deadlines several days before the sale. Missing registration means missing the auction entirely.

Capital requirements: for tax lien certificates, starting amounts can be as low as a few hundred dollars in rural counties. For tax deed auctions, you are bidding on full properties, and even starting bids in modest markets can run thousands of dollars. Understand your capital limit before registering and stick to it at auction — competitive pressure is real, and overbidding is one of the most common and costly mistakes.

Step 5 — Bid Strategically

Auction format determines bidding strategy. In bid-down interest states like Florida and Arizona, investors bid the interest rate down from the statutory ceiling. In bid-up premium states like New Jersey, investors bid above the face value of the lien. In tax deed auctions, investors bid the purchase price up from the minimum.

Know the format, know your maximum bid, and know when to stop. Properties in desirable areas attract institutional competition. Smaller counties and rural properties often offer better returns precisely because fewer bidders show up.

Step 6 — Post-Auction Actions

For tax lien certificates: record your certificate with the county if required (rules vary), set up a tracking system for the redemption deadline, and monitor the property's condition over the hold period. If the redemption deadline passes without payment, you have a legal window to initiate foreclosure. That window has a deadline too — missing it can void your rights.

For tax deed purchases: secure the property immediately (change locks, board if vacant), conduct a full title review, and decide your exit strategy. Title insurance may be difficult to obtain right away — many attorneys will not issue it until one to two years after the sale or until a quiet title action has been completed. Plan your resale or rental timeline around this.

Skip the Trial and Error Our 3-Day Workshop and live training events walk you through the entire buying process with real auction examples. See what's on the calendar. |

What Happens After You Win at a Delinquent Tax Sale?

The auction close is not the end — it is the beginning of the active portion of the investment. Here is what typically follows in each scenario.

If You Bought a Tax Lien Certificate

You receive a certificate document (physical or digital) confirming your purchase. You are now the holder of a legal claim against the property with a senior lien position. Your job for the redemption period is to monitor — track the redemption deadline, watch for bankruptcy filings (which trigger an automatic stay on foreclosure), and maintain records of all costs associated with the certificate.

If the owner redeems: the county notifies you, you receive the redemption payment, and the investment is complete. Your return is the statutory interest earned from purchase date to redemption date.

If the owner does not redeem: you file for foreclosure within the legally defined window. The foreclosure process extinguishes the owner's right of redemptionThe legal right of a property owner to reclaim their property after a tax sale by paying the full amount of delinquent taxes, interest, and penalties. and — if successful — results in a deed being issued to you. This process requires an attorney in most states and takes months to over a year depending on the jurisdiction.

If You Bought a Tax Deed

You receive a deed at or shortly after the auction close. In most tax deed states, this gives you immediate ownership. Your priority actions: secure the property, begin a title review, and determine your exit strategy.

If there is a redemption period (redeemable deedA tax deed sale where the original property owner retains the right to buy back the property within a specified redemption period. state): you own the property but cannot develop or sell it without risk until the redemption window closes. Keep the property secured and monitor for any redemption activity. If the prior owner redeems, you receive your auction price plus the statutory penalty. For more on how self-directed IRA investing can be applied to tax deed acquisitions, see our IRA investing post.

For a complete side-by-side comparison of both strategies — including which is right for your investment goals — see our in-depth guide at United Tax Liens, which covers the same strategies across an expanded curriculum format.

Risks You Need to Understand Before Bidding

Neither strategy is risk-free. These are the risks that matter most and that new investors most often underestimate.

Buying on inadequate collateral. If the property is worth less than your total costs (lien face value + foreclosure costs, or tax deed purchase price + rehab costs), you face a loss. Property condition, environmental contamination, and structural issues are real. Research every property individually.

Surviving federal tax liens. Federal IRS liens can survive a tax deed sale under certain conditions. A property with an undiscovered federal lien can become effectively unsaleable until that lien is resolved. Title research before bidding is not optional.

Bankruptcy filings. If the property owner files for bankruptcy before the deed sale or during your lien's redemption period, proceedings stop. The automatic stay halts foreclosure. You will need to work with a bankruptcy attorney to protect your position, which adds cost and time.

Overbidding at auction. Competitive pressure — especially in online auctions — drives bids up. The number that makes an investment profitable is fixed by the property's value and your costs. Paying more than that number is a loss regardless of how the auction felt.

Jurisdiction mistakes. Applying lien-state due diligence to a deed-state purchase (or vice versa) leaves blind spots. Know your state type before you start research, and apply the correct framework.

Frequently Asked Questions

Can anyone buy property at a delinquent tax sale?

In most states, any adult with the required registration and capital deposit can participate. Some counties restrict participation to state residents or licensed entities for certain sale types — verify with the specific county before registering.

How much can you realistically make?

Returns vary significantly by strategy and state. Tax lien certificates in competitive markets typically yield 8–15% annualized after bid-down. Tax deed acquisitions can generate larger absolute returns but require more capital, more due diligence, and more active management. For a detailed breakdown of how tax lien returns are calculated, see our guide on how tax lien investing yields high profits.

Do you need to be a licensed real estate professional?

No. Participating in tax lien or tax deed sales does not require a real estate license. You are participating in a government-run public auction process, not practicing as a real estate agent. Investors at all levels — from individuals to institutional funds — participate in these auctions without licensing requirements specific to this activity.

What is a quiet title action?

A quiet title action is a lawsuit filed to establish clear legal ownership of a property — typically used after a tax deed acquisition to clear any clouds on title from prior ownership, encumbrances, or potential competing claims. It is a common and necessary step for tax deed investors who want to resell or refinance a property. Most title insurance companies will issue a policy only after a successful quiet title proceeding.

Is it possible to buy delinquent tax property without attending an auction?

In some jurisdictions, unsold tax liens or deeds from a prior auction are available for direct purchase from the county through what is called an 'over-the-counterTax liens or tax deeds that were not sold at public auction and are available for purchase directly from the county or taxing authority.' (OTC) sale. These are properties or liens that did not sell at the public auction. OTC purchases can offer opportunities without the competitive pressure of a live auction — but they also often represent properties that other investors passed on, which warrants extra due diligence.

Can I use financing to buy tax deed properties?

Hard money lenders and private lenders will sometimes finance tax deed acquisitions, but traditional mortgage lenders generally will not — partly due to the title insurance problem discussed above. The practical reality is that most tax deed bidders bring cash or have cash-equivalent funding arranged before the auction. Tax lien certificates are almost always a cash investment.

Conclusion

Buying property through delinquent tax sales is a concrete process with concrete steps. The opportunity is real. So is the complexity. The investors who do well in this space are the ones who took the time to understand their state's system, researched individual properties before bidding, and bid within a number that the math actually supported.

If you are ready to go deeper on either strategy, the Tax Lien Wealth Builders beginner's guide covers the full framework for tax lien investing. Our free live events provide hands-on instruction with real auction examples — no prior experience required.

The foundation is always the same: understand what you are buying, understand what the property is worth, and understand the rules in your target state. Everything else follows from getting those three things right.

Attend a Free Live Event Tax Lien Wealth Builders hosts free educational events across the US. See real auction examples, ask questions, and learn the process from experienced instructors. |

Earnings Disclaimer Results vary. Investing in delinquent tax properties involves risk, including the potential loss of principal. Nothing in this article constitutes financial, legal, or investment advice. See our full earnings disclaimer before making any investment decisions. |

Related reading: Tax Lien vs. Tax Deed: Key Differences · How to Invest in Tax Liens · What Is a Tax Lien · Best States for Tax Lien Investing · Explore Our Blog